Zepto: The Ultimate Solution To Absolutely Nothing – Just A Thrilling Game Of Cash Burning And Colossal Funding!

Funding-Discount-Losses-Repeat, is the new game plan of Zepto, as cash is the king, and the public can be made to dance inside the IPO ring!

Funding-Discount-Losses-Repeat, And No Business model: Is zepto a solution to finding a problem?

Just in the middle of the chilly winter of November 2024 came two contradicting pieces of news:

- The quick commerce Zepto’s cash burn has zoomed to over Rs 250 crore ($30 million) per month in the last two months amid rising competition in the quick commerce space, giving an impression of downfall of the company;

- Zepto raised $350 million in fresh funding, including investments from top Indian family offices and celebrities, giving an impression of upward momentum of the company.

But think again, and you will realise that these are not contradicting headlines; instead, they are in sync with each other.

The last two years have been astonishing for Zepto. First, it became the first unicorn of 2023, giving a break to the funding winter. Second, the company received enormous funding in 2024. All this paves the way for the shining success of the quick commerce firm, as it is heading towards an IPO in the coming years. However, when you dive deep and see the rationales, you realise the glitter dust beneath the ‘shining success’.

Zepto’s founder, Mr Aadit Palicha, is often in the news, defending the merit of his business model, either through his speeches or his LinkedIn posts describing the astonishing sales of modak makers in Ganesh Chaturthi and Diwali diyas. The recent case was last month, in which he said passion over profit drives Zepto’s $5-billion success. All these may sound soothing to the ears, but passion over profit, with a doubtful business model and no unit economics, does not sound relaxing to the financial portfolio.

Why are we saying this? Let’s dive deep. We will try to decode the math of a business and compare it with Zepto to formulate equations and find the optimal solution, if it exists, as we doubt!

First thing first—what is Zepto? It is a business. So, to succeed, Zepto has to become equitable to a successful business.

Now what is a business? People may have their own perceptions of defining a business, but in general, business is something that can be built, to make money, and sustain in the long run.

What is Zepto’s business? Zepto seems to be a terrible business. There is no logic in a 10-minute delivery.

When everything shut down during the pandemic, and everyone was grounded at their homes, two Stanford dropouts came up with the idea of 10-minute delivery and pioneered the concept of 10-minute delivery in India. At first, everyone was sceptical about them, but then investors poured money like floods, and it enticed all the big players in the market to join the bandwagon.

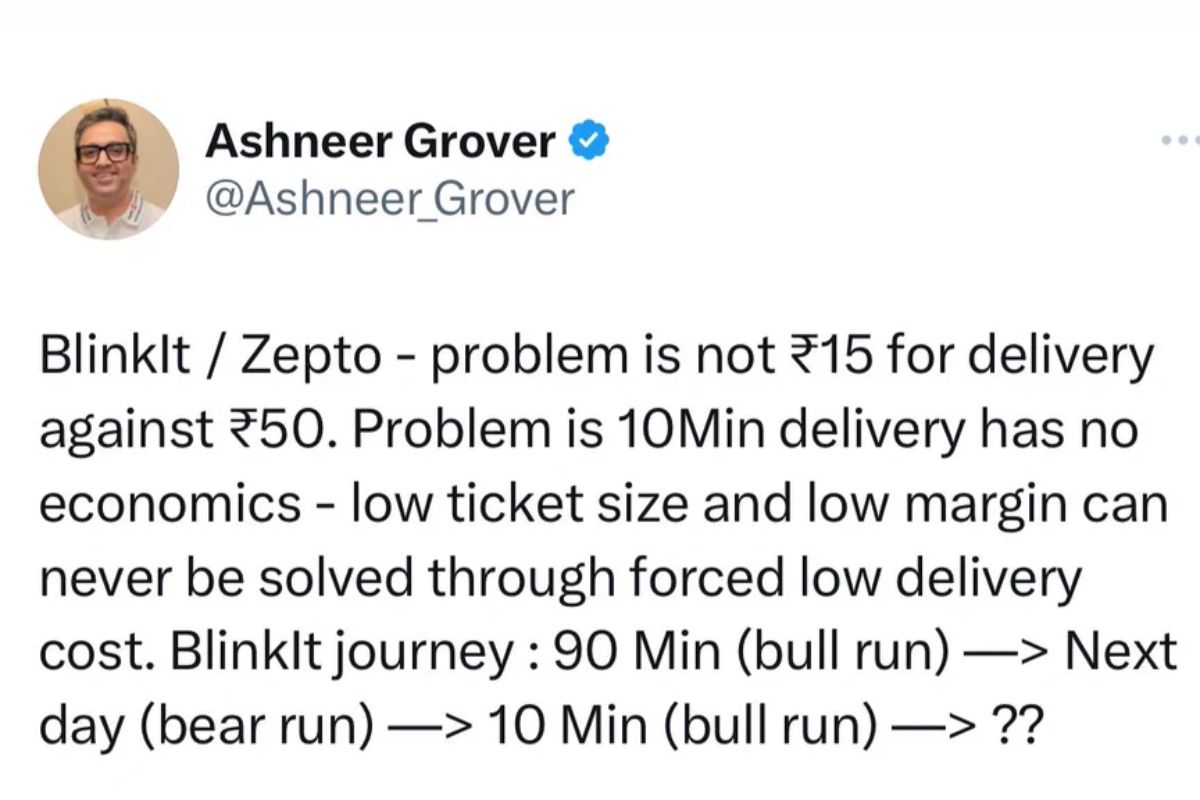

Soon, however, the shining success of 10-minute delivery faded away, and the no-unit economic model of 10-minute delivery started pinching everyone’s eyes. The very famous shark, Mr Ashneer Grover, in April 2023, came out publicly to address the idea that The 10-minute delivery has no economics. Taking to X, Grover, who previously was a core team member of Blinkit, another quick commerce player, during its Grofers days, highlighted key issues with the quick commerce delivery model, such as low ticket size and low margins, arguing that the problem with the ’10-minute’ delivery model was that it had no economics.

Mr Grover was not alone in pointing this out. Grover’s negative opinion on the economics of quick commerce delivery has another backer. Mr Hari Menon, co-founder and CEO of BigBasket, the pioneer in online grocery in India, said that consumers never wanted quick delivery and that it was thrust on them. He added that a ‘good sensible’ business that will make sense is 15-30 minute deliveries, which is what companies in this space should chase. On the growth of quick commerce, Menon added that he doesn’t think it will scale that fast. Therefore, going by the words of industry experts like the above, the 10-minute delivery will never be successful, paving the notion of Zepto as a terrible business.

Did you ever know that 10-minute delivery is ‘subject to conditions’?

In April this year, The Central Consumer Protection Authority (CCPA) reportedly asked quick commerce players Zepto, Blinkit, Swiggy Instamart, and Big Basket (BB Now) to prove their ’10 minute’ delivery claims, asking the companies mentioned above to share median data for delivery times across major cities like Bengaluru, Mumbai, Delhi, Kolkata, and Chennai. The four startups mentioned above heavily utilise the “10-minute deliveries” prospect in their brand messaging. However, this is subject to terms and conditions.

The reporting sources further cited a senior government official saying that the companies are not expected to change their messaging yet. If their median delivery times paint a different picture, they will be asked to alter their ads to reflect the actual times. So what you think of 10-minute delivery is actually, many times, a marketing gimmick! See this LinkedIn post, and you will get the facts.

Second, a business can only work when there is an audience to buy its output as a product or a service. So, will Zepto always have an audience?

The purchasing power of Indians is not so decent.

These grocery delivery services, which saw their emergence in the US, have different dynamics than those of India. In the US, the average population density is 38 people per square kilometre. On the other hand, it is 488 people per square kilometer in India. This means that Indians are over 13 times more crammed up in comparison (Maths- 488/38=12.84). In the US, a typical market is about a few kilometres away from an average household or society, while in India, it’s within a couple of hundred meters away.

Fetching a few grocery items requires some effort in the US, but it’s just a few minutes walk here. It’s not that big of a problem because of the shorter distances. Moreover, as one moves to smaller towns, the people there are still ingrained into their traditional practices of moving out and getting things from the respective brick-and-mortar outlets.

However, owing to the laziness of Indians nowadays, who are ready to pay for their convenience, we can consider that this segment will see zooming growth in the future. But is this real? What segment of people are ready to pay for such convenience?

Comparing India’s dynamics with that of the most powerful country in the world, we can see many differences. The United States’ per capita income in 2023 was $69,810, and India’s per capita in 2023 was $2,485, making a difference of 28 times. There’s a very, very small faction of people who can afford to avail of this service on a regular basis in this country. Although there is a rise in the number of middle-class people in the country, the statistics are not so high. The NITI AAYOG CEO, BVR Subrahmanyam, said in September this year that ‘The middle-income trap is the biggest threat to India’s growth’.

For the past 15 years, the incomes of ordinary Indians, those between the top 15% and 50% of the population – have stagnated. The poorest 20% see a rise in incomes due to growing subsidies and handouts. Over 120 million people between 18 and 35 are neither in education nor looking for employment. Do you think in such cases, one can avail of the ‘luxurious quick delivery service’ by choosing the ‘invisible convenience’ over ‘real, decreasing cash’? Seems doubtful.

Looking at it from an Indian perspective, when your local kirana or mom-and-pop store is just a stone’s throw away, one’s first thought is why anyone would want to order through a Quick Commerce app unless there is a compelling enough reason to do so.

Urban people, particularly in big cities and towns, already have neighbourhood kirana shops or supermarkets that provide free door delivery. Beyond free deliveries, many traditional homes have a ‘khata’ or an ‘ongoing account’ with their next-door grocer, which allows them to place orders over the phone and pay at their leisure, with no interest fee, or platform fee, or rain fee, or illegitimate charges.

So why should one opt for a grocery delivery app when they have their own kirana available in their neighbourhood? But there is a twist here. According to a report by Datum, Kirana stores’ market share fell from 95 per cent in 2018 to 92.6 per cent in 2023 and is projected to drop further to 88.9 per cent by 2028, highlighting the growing preference of consumers for online grocery shopping. But will this inclination be forever, or will it grow?

To resist this attack, kirana stores are in no way keeping quiet. Several Kirana stores are adopting innovation. Kirana store owners are trying to adapt to the digital era by utilising WhatsApp, accepting purchases online, upgrading their invoicing systems, and even redesigning their store layout and selling methods. Though the battle with quick-commerce platforms may ultimately prove too difficult to win, these Kirana stores are leaving no stone unturned. Those who have access to funds and resources and have the financial means to invest in technology or redesign their stores to attract customers are definitely going a mile ahead, and those who haven’t these are exploring the method of defining their selling strategies and prices to retain customers.

For the time being, many Kirana stores rely on long-standing relationships with customers to provide personalised care and a hands-on shopping experience that quick-commerce platforms cannot mimic. Many are writing new prices for their customers to move back to their physical outlets from the quick commerce platform.

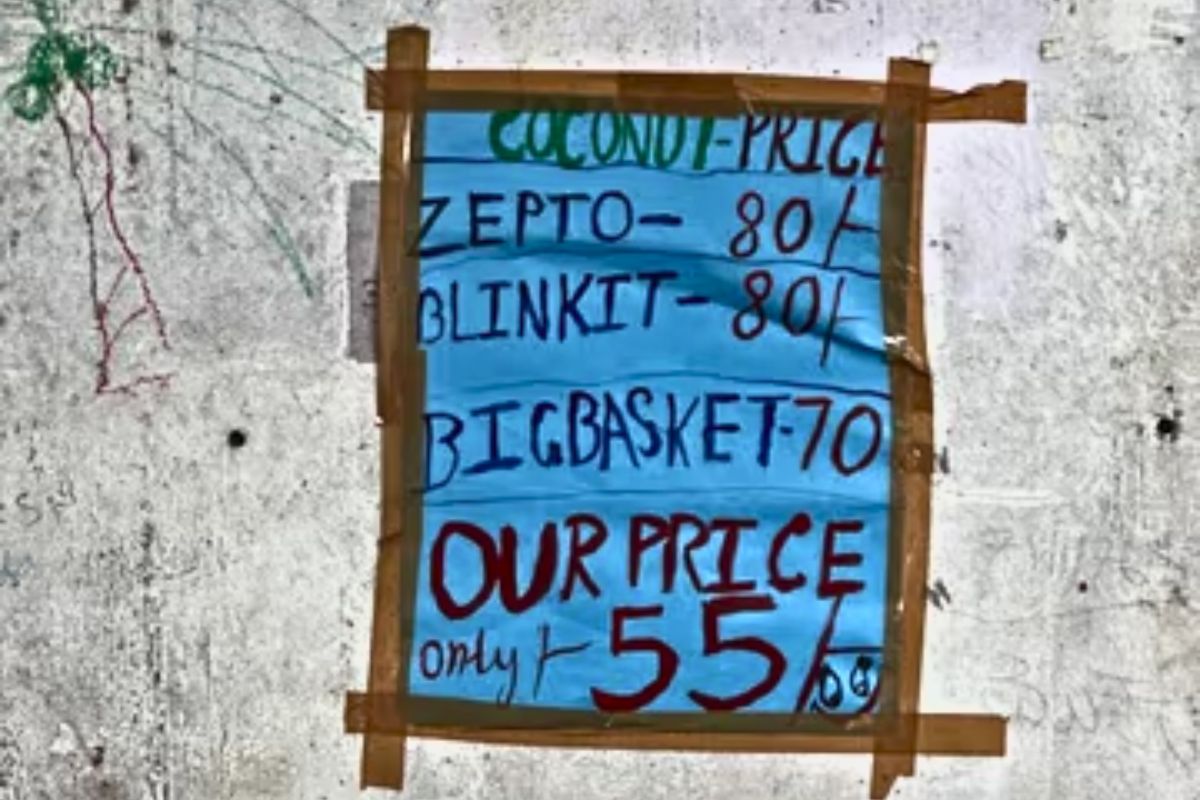

An example is from the start of the month, which can be seen in Bengaluru, where a Vendor’s Rs 50 Coconut Ad Takes A Dig At Online Delivery Giants. In what can be described as a “Peak Bengaluru” moment, a local vendor was seen offering his coconuts at a significantly lower price than the delivery platforms. His affordable pricing, as well as the striking difference with Blinkit, Zepto, and BigBasket, has become a talking point on the internet.

Though the survival of these Kirana stores is harsh, as said above, there are chances that the Kiranas are not going to accept defeat so easily, giving tough competition to the sustainability of the quick commerce companies in general and to the 10-minute delivery in particular.

Also, there is always the entry of a new player. Strategically, one problem with the industry is the low entry barriers, which implies it is easy for new competitors to keep down the profits. New apps are emerging that offer similar services by connecting customers directly with local stores. For instance, ‘My Kirana’ in Pune allows customers to order from their local Kirana stores via an app, ensuring fast delivery without the need to use Zepto. These apps pose a potential threat by taking away customers from established quick commerce platforms.

The audience of quick commerce-who are now chasing convenience, will tend to shift in reverse one day, giving a dent to quick commerce!

The biggest patrons of quick commerce are urban affluents, millennials, Gen Zs, bachelors, DINKs (Double Income No Kids), and young and middle-aged urban households who are perennially time-starved and die-hard convenience seekers. In particular, GenZs are the largest users of quick commerce, while most people above the age of 35 seem to still prefer traditional retail. One may say that Gen Z is going to be the future, and hence, the zooming pattern of Zepto and other quick commerce players will be seen moving exponentially upwards.

However, there is a catch. The so-called Gen Z and young millennials are the offsprings of Generation Y, who have worked hard enough to take themselves and their families from poor, lower middle-class levels to the decent middle-class and upper levels. Since these Generation Y candidates have seen enough financial strains in their earlier days, which have strained the dreams of many, hence they have tried to provide not only the basic amenities but also the luxuries to their offspring without any hesitation and curbed finances, which eventually made the younger millennials and the Gen Z prone to the quick commerce markets.

However, as times are moving and these younger millennials and the Gen Zs are trying to stand on their own feet and enter the maturing stages of lives, they are supposed to become more conscious about their finances and may not opt for choosing convenience and speed, that is the only core offering of this quick delivery and 10-minute delivery segments.

As these young cohorts will enter into the mature stages of parenting and saving, they are expected to divert these funds of convenience shopping towards the education and lifestyle arrangements. Therefore, the viability of the quick commerce segment and the 10 minute delivery will again be seen under the sword of survival!

As Generation Z grows and develops expertise in finances, they may become less impulsive in their purchase decisions and behaviours. Quick commerce, which relies on quick pleasure, may be less appealing to them than it was when they were younger. They may choose to plan their purchases more carefully, using traditional retail or subscription arrangements.

Furthermore, as these young cohort become more financially independent and concerned about the environment, they may move with brands that promote sustainability. Quick commerce, with its emphasis on speed and the significant carbon footprint associated with fast delivery, may be less desirable if these services do not line with their environmentally conscientious beliefs.

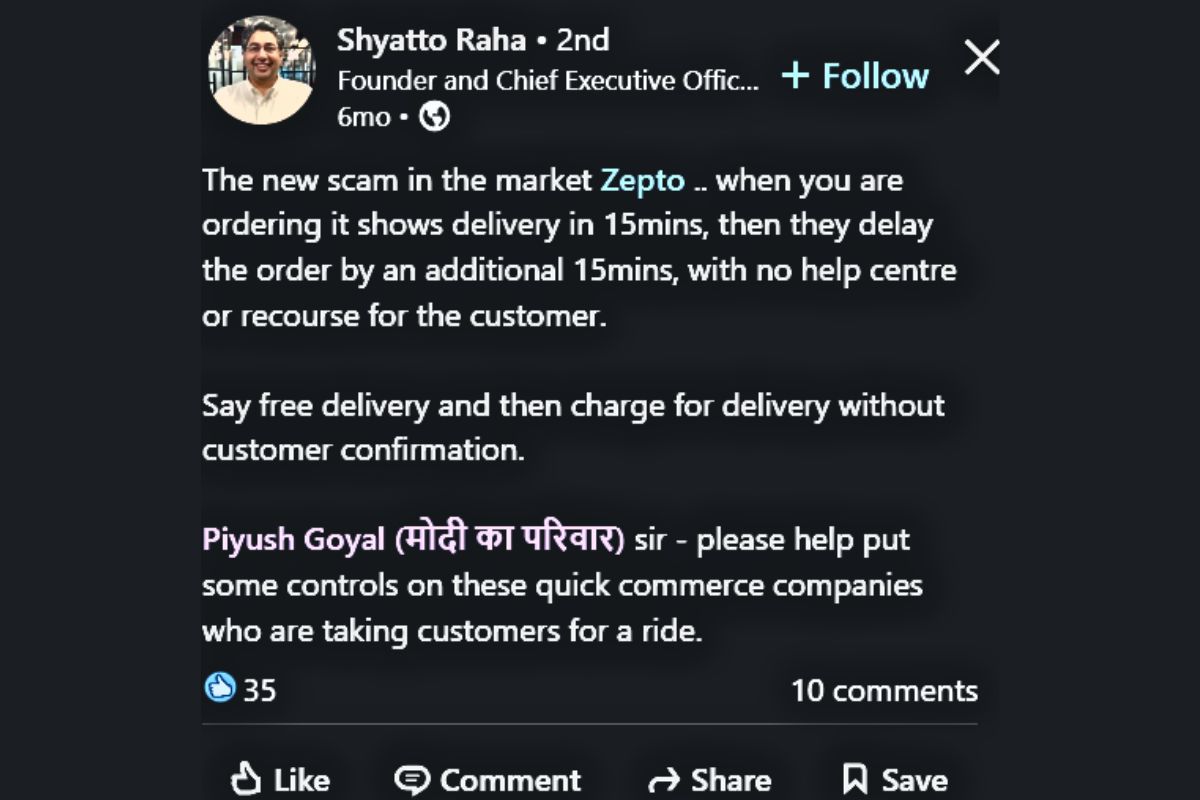

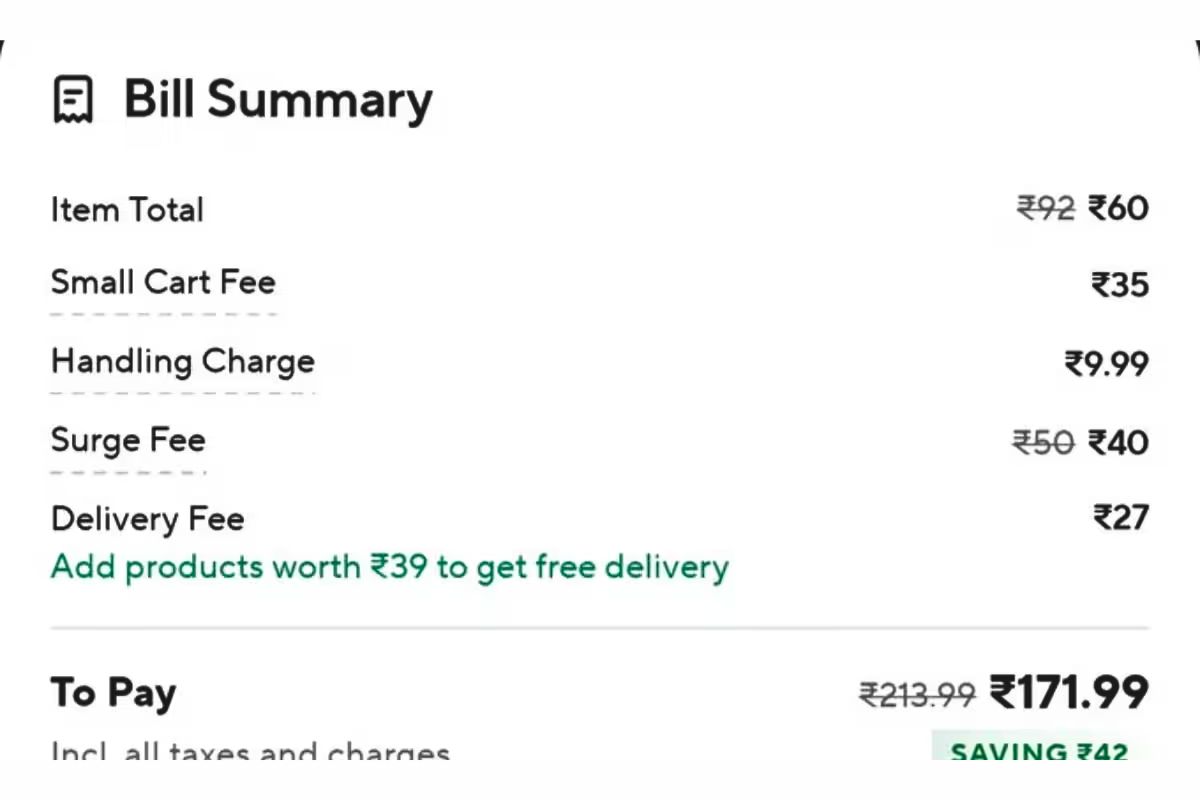

See this example from September 2024, where a Zepto User’s Rs 60 Order Comes With Rs 112 Extra Fees. Netizens were quick to cry about the ‘scam’. So, do you think there will always be an audience for whom the convenience over cash will be so great that they pay double for the price of the product purchased? Think!

Also, with the large behemoths offering free delivery services, customers will eventually become hesitant to pay for delivery charges, especially in the above case. Customers are so sensitive to delivery charges that they will even look around multiple options before finding one that isn’t charging any. Consequently, startups are forced to offer free deliveries or risk losing clients.

Navneet Singh, CEO and co-founder of PepperTap, which was the third largest grocery delivery startup in India (with USD 50 million in raised capital) before it exited the business in 2016, cited this issue as one of the chief reasons why this vertical isn’t working in India.

Third- There is nothing more than discounts.

Not only Zepto but every other company is playing on discounts. It seems that a discounting war can be seen between companies. These businesses often suffer from a lack of customer loyalty, and the grocery delivery vertical is no different. Customers do not really care which startup they are ordering from. All they care about is how much it costs them. So often, it comes down to which brand offers more discounts. The customer will just keep shifting from one option to another depending on where they are getting more discounts. This degenerates the entire industry into cutthroat discounting and price wars.

Today’s consumer is more concerned with the cost supplied by using the brand rather than the logo itself. Because the consumer is loyal to the price supplied by the brand rather than the logo itself, continually improving the pricing proposition is the only option left for firms to survive in the market. Talking about Zepto, there is no doubt that they have spent enough in acquiring customers.

Not only about acquiring new customers, zepto is has been offering lucrative salary hikes to attract employees from competitors like Swiggy Instamart, Blinkit, and other quick-commerce boys. In addition to its talent-focused strategy, Zepto has been spending heavily on marketing, with nearly ₹120 crore of its monthly cash burn allocated to digital marketing alone. Therefore, the sustainability of companies like Zepto is prominently based on cash burning and, colossal funding and nothing more, at least as of now.

Fourth- Operational efficiency seems to be zero at zepto!

Zepto is an operational nightmare. It’s tremendously expensive, insanely messy, and very “people-heavy.” It’s not only people; it’s also quite capital-intensive. Every dark store in this firm costs something, and if you look attentively, the prices are enormous! Space, labour, machinery, training, packing, delivery vehicles, and so forth! Zepto’s overall costs for FY23 were Rs 3,350 crore, up from Rs 533 crore in FY22. The establishment of around 100 new stores accounted for a significant amount of these costs.

Moreover, as Zepto plans to enter into tier 2 and tier 3 cities, which have even more congested spaces, this problem of dark stores will emerge even bigger, as the presence of dark stores in dense neighbourhoods can torment residents due to the nuisance value. Affordable spaces are becoming increasingly scarce, and in September 2024, brokers noted Blinkit, another quick commerce, was actively looking to expand its dark store presence in Bengaluru but is struggling to find available properties. If problem arises with the market leader itself, then sooner or later, it will take zepto it its arms as well.

Then, the 10-minute delivery, as mentioned earlier, is also a compromising model in itself. In the case of e-commerce, which was the pioneer of online delivery, the delivery time is generally 2-3 days. The deliveries are clubbed together location-wise, and the delivery executive travels through the locations to deliver them on a single trip. Also, in case of extended delivery times, like 30 minutes to 1 hour, a delivery executive can load a maximum of 10 orders in his bag, he’ll set off to sail when he gets those 10 orders and deliver them in one single round trip. This way, the number of deliveries per person per day will increase.

However, in the case of 10-minute delivery, the delivery executive has no choice but to take a separate trip (starting from the hub) to deliver every single order, making the number of deliveries per day less. Moreover, on paper, there are no piss breaks, heatstrokes, bike malfunctions, accidents, navigation errors, etc., counted.

Also, quick commerce apps are frequently used for small, spontaneous purchases. For example, someone making a sandwich might order just bread, cheese, and tomatoes. These small orders make it challenging for companies to turn a profit. If companies try to impose a minimum order value, they risk diminishing the convenience factor that attracts users to quick commerce in the first place. Although there have been sales of electronics, iPhones, and even gold coins through Zepto, how much these products will benefit zepto is a point of question. So, betting on a 10-minute delivery seems doubtful!

Conclusion.

If there is no definite point of satisfaction that justifies the existence of quick commerce and 10 minute delivery, then why investors are injecting funds to zepto like anything?

Not only investors but also big family offices and celebrities in India are pouring their money into Zepto. Why? Big players are looking for these fledgling 10-minute delivery startups, such as Zepto, to float on the stock exchanges so that they can cash cows before it is known whether the model will ever make money. Currently, these services are majorly funded by venture capital. However, without profits, as there is no sustainable business model of 10-minute delivery, funders may quickly find these operations less appealing. Then, when cash ends, either the startup will nearly shut, as seen in the case of Dunzo, or there is a more appealing route- the IPO!

Funding-Discount-Losses-Repeat, as cash is the king, and the public can be made to dance inside the IPO ring?

Wait, let me tell you, the above appeal factor is for the investors and the startup owners and not for the general public. In the end, investors will take multiple sums of returns from their cash procured into these companies, and hence, since the business model is nothing but cash burning and colossal funding, in the end, the retail investors and general public will bear the brunt of these cash collapses, via the route of IPO.

And if, these services, companies like Zepto survive, as a result, these services are only likely to operate in areas with high-density affluent populations in big cities like Delhi, Bengaluru, and Mumbai, or where there is affluent public, way farther from the middle-income class, making the startup a zombie startup.