What disruption will API banking bring to India’s banking industry in 2022?

New-age fintech businesses are now causing many changes in the financial services industry. Indian banks have made their application programming interfaces (APIs) public, allowing third parties to build on them, innovate, and provide new goods and services. As a result of the transition, the way financial goods and services are generated, delivered, and accessed has changed dramatically.

Fintech companies have taken advantage of this chance to introduce automation to continually provide a consistent consumer experience. This also enables them to perform banking operations and access banking data to develop new creative financial services. Customers can use them to complete transactions, check account information or balances, apply for loans, and receive payment instruments such as cards, among other things.

Let’s look at an example:

- PayTransfer, a third-party fintech company, has been granted access to ABC Bank’s main banking system.

- PayTransfer works with the API of ABC Bank. They will be able to connect to the bank’s basic banking system due to this.

- PayTransfer performs API calls (essentially requests) to the ABC bank’s server to perform financial activities or retrieve information.

- Businesses may access numerous bank APIs and deliver financial services using a single PayTransfer API.

What are APIs?

APIs are a collection of standards that make data transmission between two apps simple and safe. These serve as an intermediary layer, allowing data to flow between the two apps and allowing the two parties to benefit from each other’s data. Any third party, such as a tech firm, a corporation, or a fintech player, can access a bank’s core banking system to execute banking operations via APIs.

API-led banking has ushered in a substantial shift in how financial operations are carried out today by offering simple access to banking services, products, and data. Account opening, cash transfers, lending, card issuance, and other core banking services can be unbundled and made available to third parties.

APIs assist banks in the following areas:

- Meet the evolving demands of current clients while also attracting new ones.

- Improve client satisfaction with new BaaS products.

- Ensure that banking procedures are safe, flexible, and future-proof.

Third-party inventors have greater freedom to:

- Better banking features and financial services should be available.

- Increase the number of new fintech products available on the market.

- Obtain a competitive edge

From the perspective of a client, they can:

- Banking transactions may be completed anywhere, not only from their bank or bank app.

- Get tailored financial service offerings when consumers need them, such as credit offers at checkout or wallet payment options (gig workers)

- See a consolidated picture of their money from a single dashboard and control, track, and analyze financial movements.

Banking as a service: fostering a collaborative age

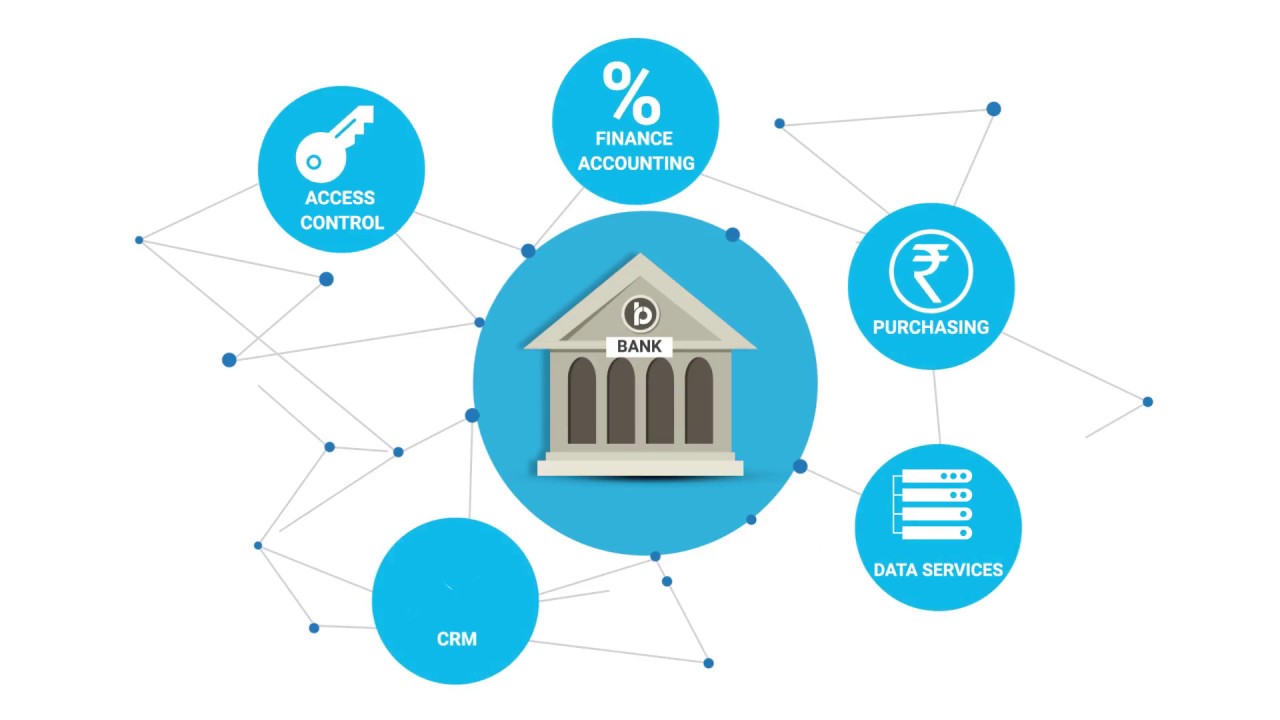

Non-banks are developing and providing many fundamental financial services to clients by connecting with bank APIs. Platforms that provide banking-as-a-service (‘BaaS’) as middleware or an API-based BaaS layer are emerging. On the back end, this intermediate layer connects with banks and other regulated entities, while on the front end, it hosts a variety of fintech startups and non-bank enterprises.

Various may be considered lego baseplates that these entities can ‘plug and play’ into. The underlying banks and other partners provide the regulatory foundation, the API platforms offer infrastructure, and fintech and other non-bank enterprises integrate financial services into their non-financial goods.

Open-banking API services are being actively used by fintech and others to:

- Provide real-time account balances

- High-speed payment processing for vendors

- Reduce administrative and other barriers to credit provision, such as applying for a company loan, determining credit eligibility, and so on.

- Assist in the issuance of cards, wallets, and other items.

- Cash position, cash flow, and other financial data are now more visible.

With new products and services at their disposal, the end consumer emerges as the largest winner. They also benefit from a great customer experience at a low cost. Non-banks gain from the freedom to refocus on key business offerings, which fosters innovation and faster market time.

Financial services distribution and a future roadmap

The success of BaaS is heavily reliant on banking and other stakeholders providing the necessary underlying regulated layer. Banks must make important efforts to enable collaborative innovation, such as modernizing their existing technology stack, providing APIs, and facilitating third-party integrations. Here, security is critical, needing actions such as effective identity and access control and secure data transfer protocols.

Banks will progressively outsource the distribution of their financial goods and services to third-party fintech and others, changing the responsibilities of various stakeholders in the BaaS ecosystem.

Third parties will be in charge of innovating to develop consumer engagement and satisfy new-age expectations through personalization and value-added services. These third parties will assist banks in expanding their client base and reaching out to previously untapped markets.

For all stakeholders, BaaS has opened up a wealth of possibilities. Accounts, issuing cards, investing, lending, and other services accessible through such collaborative third parties– this is fintech’s next big bet! It has undoubtedly opened up interesting opportunities in the financial industry. Open banking, embedded banking, co-lending, account aggregation, and API-driven financial infrastructure will all see significant developments in the future.

It is important to recognize that for a diversified economy like India, which has a wide range of financial demands, collaborative – rather than competitive – efforts are required to meet those needs. BaaS facilitates this by establishing a win-win scenario for all players — banks, non-banks, and end customers. The financial services environment will change as APIs, and API banking grow.