The Uprising of Fintech Companies in India in the 21st century

A FinTech company was initially defined in the 21st century as a technological alternative to traditional financial companies’ back-end systems. FinTech encompasses various sectors and industries, including education, retail banking, non-profit fundraising, investment management, and many others.

FinTech provides financial process and operations management through specialized software and algorithms. A large part of FinTech today still focuses on the traditional global banking industry, despite various sectors of FinTech gaining traction. Developing and using cryptocurrencies like Bitcoin has also become part of FinTech. One of the leaders in this revolution in India.

Fintech – What Is It?

Described as new tech that aims to improve and automate financial services, financial technology (Fintech) incorporates new ways to provide and use financial services. Fintech relies on specialized software and algorithms used on computers and, increasingly, smartphones to help companies, business owners, and consumers manage their financial operations, processes, and lives. “Fintech” combines “financial technology” with “technology”.

In the early 21st century, fintech denoted technology used by established financial institutions to power their back-end systems. Since then, however, consumer-oriented services have become more prevalent, and hence the definition has become more consumer-oriented. In addition to education, retail banking, fundraising, nonprofits, and investment management, Fintech now includes many other sectors.

Crypto-currencies like bitcoin are also part of Fintech. This fintech segment may receive the most attention, but the real money is still hidden in the multitrillion-dollar market capitalization of traditional global banks.

Why is India leading a fintech revolution?

One of India’s fastest-growing technology segments is Fintech, which delivers loan applications, payments, stock trading, and credit scoring innovations. India’s fintech adoption rate is the highest worldwide (87%) and is the most important investment destination.

Mumbai, Gurugram, Bengaluru, New Delhi, and Hyderabad are some of the top fintech destinations in India. Fintech hubs in India are centred in Mumbai and Bengaluru, each contributing 42%.

FinTech companies are transforming the sector rapidly by digitizing services and implementing paperless and cashless processes in the banking industry. In case you don’t know, FinTech refers to digital innovations aimed at improving and automating the delivery of financial services. FinTech comprises both “financial technology” and “financial.”

Increasing FinTech use in India

As its economy has grown at one of the fastest rates, India has become a hotbed for FinTech. Several technologies have already been implemented in India, such as mobile banking, secure payment gateways, mobile wallets, etc.

Digital payment systems have been widely adopted in India over the last two years, making essential financial services a lot more convenient. Several factors have contributed to the growth and expansion of the FinTech industry in India, including the increasing availability of smartphones and internet access and faster internet speeds.

Based on a Boston Consulting Group and FICCI, India’s FinTech sector is expected to increase in value by USD 100 billion by 2025, meaning that India will create USD 150-160 billion in incremental value. This report titled India FinTech: A USD 100 Billion Opportunity says that India will need $20-25 billion in investments to reach its goal over the next few years.

Impact Analysis of COVID-19:

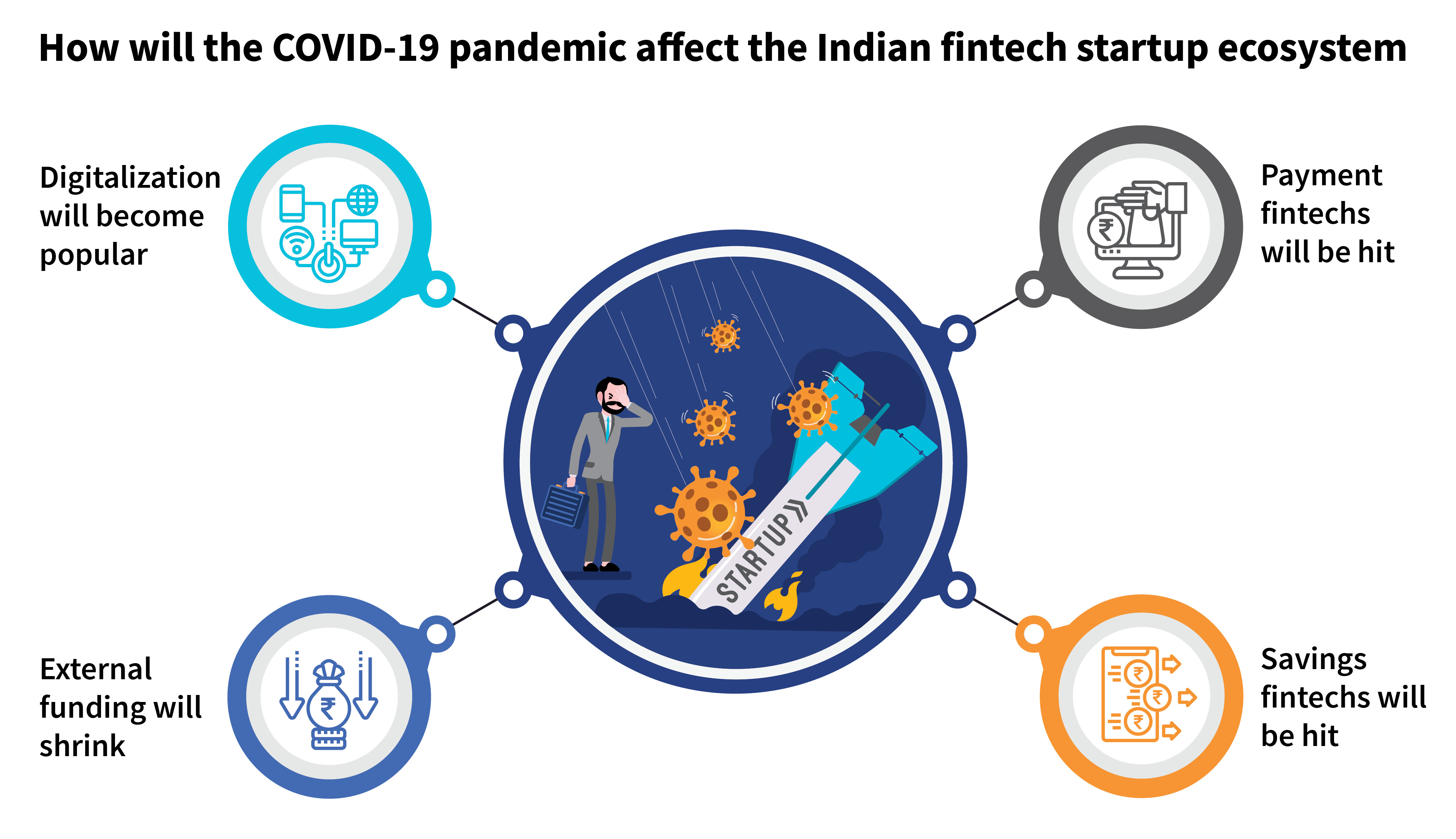

The pandemic has benefited the fintech market. After the pandemic started, the fintech sector became the front line of the country’s struggle for financial inclusion. Payment and lending systems proliferated. During the lockdown, a 40% increase in digital transactions was recorded.

People began to use cashless and digital payment methods because they were afraid of public gatherings. People increased their adoption of life and health insurance, leading to growth in the InsurTech segment.

A closer look at India’s FinTech Companies

Banks have traditionally handled payment services in India. As technology advances rapidly, this no longer appears to be the case, as banks gradually lose their monopoly in this area.

India has seen significant improvements to its payments infrastructure over the past few years, thanks to its introduction of new payment mechanisms and interfaces such as the Immediate Payment Service (IMPS), the Unified Payments Interface (UPI), the Bharat Interface for Money (BHIM), and others.

In addition to the Make in India and Digital India programs, the government’s initiatives significantly accelerated the uptake of Fintech companies. It is very commendable that the Reserve Bank of India (RBI) has also pushed the establishment of a cashless society by increasing electronic payments.

Moreover, the demonetization and GST initiatives implemented by the government have provided an ample amount of opportunities for fintech development. The demonetization process resulted in some chaos and frenzy in the general public.

Still, ultimately, it accelerated the nation’s already-existing FinTech revolution by shifting the economy from a cash-based to a digital, electronic one. Therefore, we can assume that the COVID-19 pandemic has accelerated this digitalization across numerous categories, promoting contactless and cashless payments to discourage social interaction.

India has seen 10-15 million customers jumping on the digital bandwagon in the last 12 months, and digital payment methods have become a way of life. Demonetization and the Covid-19 pandemic were both factors that led to this change. According to the report, over 67 per cent of India’s 2100 FinTech companies were founded within the past five years.

Digital payment systems have undeniably emerged as the flag bearers of the Indian FinTech market, courtesy of platforms such as PayTM, PhonePe, MobiKwik, etc. As part of the partnership, Facebook and Reliance Jio will focus on hyperlocal e-commerce in rural and remote locations and tier 2 and 3 cities. This will transform India’s digital payments sector.

FinTech Companies in India: the future

Despite its vast diversity and population, a large part of India remains underbanked, underserved and constantly subject to changing regulations. Because of these factors, overcoming the nation’s financial challenges and unresolved issues will be no easy task. With Fintech’s ability and power to fundamentally alter and transform India’s financial and banking services, Fintech enters the equation.

The country offers an excellent setting for a FinTech revolution because of several factors, including an innovation-driven startup scene, a highly favourable market, high smartphone and internet penetration levels, and a young, urban population with a median age of 25. Moreover, the growing awareness of financial technology has provided a much-needed boost to the Indian FinTech sector.

In India, the growing partnerships of FinTech industry companies with traditional financial institutions such as banks, insurance companies, and retailers, where these companies are actively catering to changing customer needs, will accelerate FinTech expansion.

Looking at all these factors, the industry has vast growth potential, with the country gearing up for widespread adoption of FinTech.

Top 10 FinTech Companies in India

- Lendingkart

In 2014, Harshvardhan Lunia and Mukul Sachan founded Lendingkart, an online financing company. Throughout India, small and medium-sized businesses can access working capital loans and company loans from Lendingkart Finance.

With complete online access and minimal documentation, they quickly provide capital without collateral. To help entrepreneurs deal with their cash flow gaps, the company gives them access to capital funding at their fingertips. The companies are based in Ahmedabad, Bangalore, and Mumbai, but they serve the entire country.

- MoneyTap

MoneyTap offers a credit line based on an app. Anuj Kacker, Kual Verma, and Bala Parthasarathy founded MoneyTap in 2015. Cash loans for minor to medium businesses, fast mobile credit, flexible EMI plans, and competitive interest rates are offered by MoneyTap.

Using an application, anyone with a smartphone and a PAN can find out how much cash they qualify for in less than 15 minutes. Except for certain documents required by the partner bank’s KYC legislation, the entire process is entirely paperless. It’s interesting to note that interest rates only apply to the amount you borrow, not the whole cap you agreed to accept. With MoneyTap, we also operate with NBFCs in India that have RBI licenses and are regulated by the RBI.

- Instamojo

Aditya Sengupta, Sampad Swain, and Akash Gehani founded Instamojo in September of 2012. To boost your business, Instagramojo collects fees, creates free online stores, ships goods, gets loans, and more.

Through our suite of services, including payments, free online stores, logistics, credit and finance, and more, micro-entrepreneurs, startups, small and medium-sized businesses, and others are using Instamojo to start, market, run, and expand quickly. A company can expand online using Instagramojo’s personalized business tools.

- Razorpay

Razorpay is an Indian payment solution that facilitates the receipt, processing, and disbursement of payments for companies. Payments options include JioMoney, Mobikwik, Airtel Money, FreeCharge, Ola Money, and PayZapp, in addition to credit cards, debit cards, net banking, and UPI. Shashank Kumar and Harshil Mathur founded the organization in 2014. The platform lets businesses manage the marketplace, conduct money transactions, receive regular fees, exchange invoices with clients, and apply for working capital loans.

- Paytm

A company owned by One97 Communications and approved by the Reserve Bank of India Paytm was founded by Vijay Shekhar Sharma. Paytm is connected to many companies, including Uber, MakeMyTrip, BookMyShow, Foodpanda, etc. The company has Softbank, Ant Financial, AGH Holdings, SAIF Partners, Berkshire Hathaway, T Rowe Price, and Discovery Capital. One97 Communications Ltd (OCL) is the wholly-owned subsidiary of Paytm Insurance and is an IRDAI licensed insurance brokerage.

- Policybazaar

Avaneesh Nirjar, Yashish Dahiya, and Alok Bansal founded PolicyBazaar in Gurugram in June 2008. The world’s largest fintech company, Policybazaar.com, is India’s largest insurance aggregator. It serves as a pricing comparison tool and a knowledge base to let users find out more about insurance as an online platform. Later, it became a marketplace for insurance policies. Through the advertising and promotion of insurance providers on the organization’s website, revenue is generated for the organization.

- Shiksha Finance

India’s largest education finance company is Siksha Finance. This institution aims to reduce school dropout rates by funding parents’ school fees. Approximately Rs 10,000 to Rs 30,050 must be returned within six to ten months. In addition to paying for school tuition, books, uniforms, shoes, luggage, and so on, parents can use student loans for other purposes. Educational institutions can also use the loans to develop buildings, buy properties, and finance working capital.

- PineLabs

Pine Labs has released its full range of products in Malaysia since 2017. The company was founded by Lokvir Kapoor, Rajul Garg, and Tarun Upaday in 1998. You can accept any digital payment with this app using your NFC mobile phone, including a primary ‘Tap n Pay’ card.

Retailers are now offered various payment options, risk assessments, multi-channel analytics, leasing and insurance, brand offerings, cashback, and automated billing through the network. Over 100,000 merchants in India and many other countries in Asia use Pine Labs’ technologies. Over 350,000 PoS terminals in more than 3,700 cities are powered by the company’s cloud-based technology in India alone.

- ZestMoney

Ashish Anantharaman, Priya Sharma, and Lizzie Chapman founded ZestMoney in 2015. In ZestMoney, mobile technologies, digital banking, and artificial intelligence are combined to improve the lives of millions of Indians. The World Economic Forum named ZestMoney a 2020 Technology Leader for their groundbreaking technologies and efforts to make digital finance more accessible.

- ePayLater

The founders of ePayLater are Akshat Saxena, Aurko Bhattacharya, and Uday Somayajula. Regular online purchasers have a 14-day interest-free credit limit with ePayLater, a digital payment solution offered by Arthashastra Fintech. In addition to IRCTC, PVR, MakeMyTrip, Yatra, EaseMyTrip, Tata Croma, and Travelyaari, EPayLater has partnered with various other companies. The service is collateral-free, and there are no hidden charges. The result is a reduction in inventory time, which helps businesses deliver services to their clients while generating more sales.

Indian banking is being transformed by fintech.

India’s Fintech industry has faced several challenges despite impressive growth, including data security risks, varied adoption, rapidly changing requirements, and limited financial literacy.

Fintechs are trying to become banks, and banks are trying to become fintech, which is a very famous saying in the financial services industry in India. Although it may seem that traditional players are racing against non-traditional ones, in actuality, it’s the customers that win!

Since every player is striving to provide faster, safer, and cheaper services to the end-users while meeting increasing customer demand for inclusive financial services and reducing costs.

However, let’s begin by taking a step back to see how fintech is affecting banking. According to an interesting fact, fintech is a term coined in the 21st century to describe the technology used by established financial organizations to operate their back-end systems.

Today, the Fintech sector has transcended those boundaries and spans a variety of industries, including education, retail banking, non-profit fundraising, investment management, and many more.

A total of $4.6 Bn was raised across 160 deals in India’s fintech startup ecosystem in H1 (January to August 202), 5.8x higher than the prior year.

Indian banks are also transforming as this fintech disrupts and changes the Indian banking industry significantly. To compete with the new generation of financial players, they heavily invest in digital technologies and services.

Several government policies have been implemented to encourage the revolution, such as providing social services, transferring money, and formalizing banking systems. Indian banks are increasingly required to keep pace with India’s growing digital citizenry and create new, uniquely Indian products, services, and business models that leapfrog far ahead of the fintech.

Fintech in India has been confined to the more significant tier 1 city over the years. Fintech innovation has penetrated India’s smaller towns and cities with the COVID-19 pandemic and digital penetration.

Fintech trends

Financial Technology (Fintech) has evolved from the new kid on the block to become a standard in the financial sector. Businesses and technology have become increasingly intertwined, and startups and banks have come to appreciate the importance of technology innovation and are developing new products and services for their clients.

Shortly, the following trends are likely to bring significant change to the industry:

1. In India, FinTechs, banks, and other corporations are vying to develop India’s first SuperApp, which has gained tremendous popularity since the success of Gojek (Indonesia), Alipay (China), Rappi (Latam), and Revolut (USA).

2. Buy Now Pay Later (BNPL), and credit line disbursement to niche segments are reimagining credit and giving Indians access to digital credit at the point of purchase and enabling them to surpass traditional credit cards.

3. Millennials and employers are responding to insurtech’s invention of products and digital distribution, increasing the penetration of insurance products.

4. Fintech’s digital lending business model is maturing and focusing more on collections.

5. The rise of Neobanks has been attributed to hyper-personalized banking for the most tech-savvy segments of the consumer market. Neobanks offer accessibility, multiple banking and financial functionality that are cost-effective under one umbrella. The future lies in neobanks building niche solutions for blue-collar workers and thin-file MSMEs who are underserved.

6. This year’s COVID brought us a surprise package on wealth/invest-tech. Due to its affordable and inclusive services, it is transforming the investment landscape and attracting many first-time equity investors.

7. Banks have always shied away from Crypto trading, even though speculation has been rampant about whether it is legal in India. The latest information on the Cryptocurrency bill 2020 states the government plans to tax cryptocurrency investments instead of banning them outright, which could provide opportunities for some emerging fintech companies.

7. Fintech features like API/Smart API banking, embedded banking, and Banking as a Service (BaaS) make it possible for every company (whether financial or non-financial) to leverage the Fintech ecosystem. As a result, various platforms are also being cross-promoted.

8. MSMEs are the next battleground for Fintech (after millennials). Banks and startups alike are vying for a share of the pie. MSME have increasingly adopted digital, making the market ripe for disruption due to COVID19.

9. Payment gateways (like digital payments) continue to attract large amounts of funding, and the number of firms in IPO and unicorn queues is at an all-time high. Issuers are now acquiring payments. Payment continues to serve as a hook for players to generate revenue from cross-selling other financial services with reduced margins.

Although it has encountered a few setbacks and challenges, there has been remarkable growth in India’s Fintech industry. These include data security and privacy risks, varied adoption, rapidly changing regulation, and lack of financial literacy.

India’s fintech sector is not only one of the most dynamic segments of our economy, but it’s also something that’s being watched from all over the world! Shortly, several fintech products will find mainstream adoption, most of them into banking, backed up by blockchain, artificial intelligence, machine learning, and data analytics. In the years to come, a product that is yet to be released or under the paradigm of uncertainty may become the fundamental building block of certain banking services.

Conclusion

Keeping an eye out for upcoming top fintech companies is a result of studying this list of top Indian fintech startups.

Traditionally, all of this cash has been the biggest bottleneck in business and personal finances, but that is no longer the case. You can now make use of a new technology called Fintech. Fintech is going to grow and get better as time goes on.

Be sure to keep an eye on Fintech to see what exciting things lie ahead.

Edited and Proofread by Ashlyn Joy