Byju is an edtech, and Zepto is a quick commerce.

One may argue that why we are comparing both. However, when one deep dives, they may see similar patterns of operations in both the startups, one the poster boy of edtech and another the poster boy of quick commerce.

The desire to remain at the top and the attitude of Raise fast and burn fast and growth at any cost!

The mantra of ‘raise fast and burn fast’ is an eerily similar story found in many startups. The growth at any cost is the new fantasy of new age entrepreneurs.

Taking the example of Byju, who was once the poster boy of edtech, is nothing but worth 0 today. Why? Byjus was once the pioneering name in the field of the Indian edtech ecosystem. During covid, when every school/college was closed, Byju took the opportunity of online classes and started expanding its wings. Everything was going well, but things started showing gloomy patterns when the edtech giant developed the untamed desire to remain at the top at every cost. It continuously raised their funding and acquired every other startup in the similar domain. Byju continuously used the funds to remain at the top at every cost, which eventually contributed in one way to its liquidity crunch.

A similar attitude and desire to remain at the top can be seen in the case of Zepto. It was reported in the middle of last month about how Zepto is poaching workers from Instamart, Blinkit, and other rival firms to win the quick commerce war. This aggressive talent acquisition approach is part of Zepto’s larger strategy to outpace its competition and solidify its position as a leader in the space.

Zepto’s monthly cash burn has skyrocketed to ₹250 crore ($30 million), with a significant portion of this budget allocated to hiring and retaining top talent in the industry. This comes at a time when the race in the quick-commerce market is heating up, with major players like Swiggy Instamart, Blinkit, by Zomato, and BigBasket, by the Tatas also pouring resources into expanding their offerings.

This untamed desire to remain at the top or the greed to be an industry leader, by fuelling cash burn and keeping unit economics at the rear seat can be considered enough to compare Zepto’s race with Byju’s fate!

Unethical practices, hidden agendas.

Recall the matter of allegations of unethical practices in Byju that popped up in the news a year ago and how easily it spread like a jungle fire, only because everything behind the allegations was true. Byju not only used its deceitful tactics to acquire customers but also exploited its own employees through its toxic work culture. Keeping hidden costs while purchasing Byju products and attaching loans in the name of parents without their consent are regarded as high level of deceitful practices by Byju. An article titled ‘Loss after loss’: Parents detail how Byju’s pushed them into debt‘ published in January 2023 justifies the statement above.

Also, enough publications are there in public domain to justify how the toxic work culture at the edtech giant hurted the employees- they were asked to complete their targets at any cost, not to mention the targets were insane.

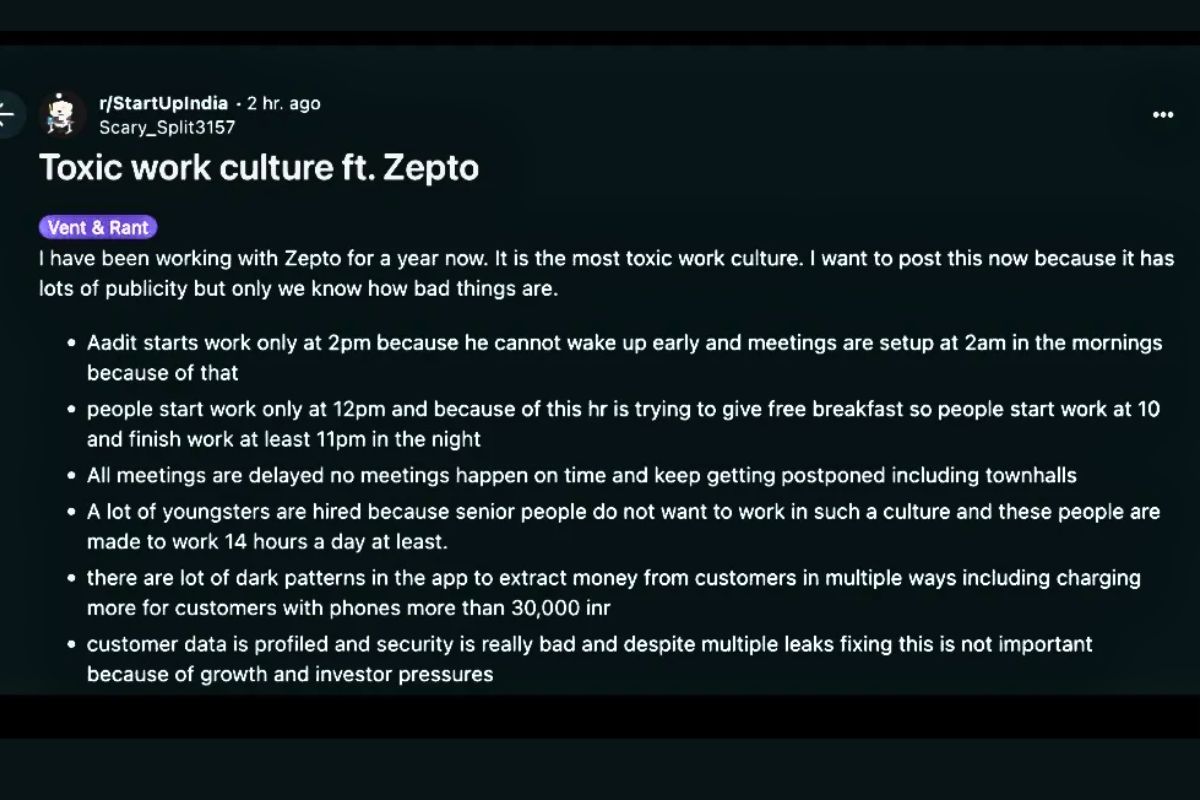

Similar waves of hidden tactics and crooked practices can be sensed in Zepto as well. Recently, a post went viral on Reddit and the Linkedin community where the hidden charges levied at the customers and the toxic work culture in zepto was highlighted.

Zepto pass is a scam- In July 2024, an article titled ‘Bengaluru Zepto subscribers users charged delivery fee despite buying a pass flag dark pattern: Robbery‘ shows how a dark pattern or a user interface has been carefully crafted to trick users into doing things, or as it appears in the delivery app’s case, trick subscribers into paying the delivery fee unless they manually opt for the free delivery. This is a testament to prove that the viral post has real facts describing Zepto’s hidden strategies to trick customers, similar to what was seen in Byju.

Another article from December 2024 titled ‘Zepto charges higher for customers with phones worth over ₹30,000, claims viral Reddit post‘ shows the quick commerce platform uses dark patterns in its application to extract money from customers in various ways. The person, claiming to be an employee, also alleges that the company profiles the customer data and that the security of the profile is “really bad”. The post further claimed that despite multiple leaks, the company did not fix this issue because of growth and investor pressures.

Moreover, the post highlighted the toxic work cultures at Zepto, including the long working hours, 2 AM meetings, etc. It syncs with Zepto CEO’s words from the October 2024 NDTV World Summit 2024, where he said that his employees often work 80–100 hours per week. Therefore, combining the words of the CEO himself and the post by Reddit users criticising toxic work culture draws parallel lines with what can be witnessed in Byju.

Lack of transparency- The false narratives the company is showering to the public on the pretext of growth.

Recall how Byju’s auditor resigned in September 2024 because of a lack of transparency. Although a year-long probe by the Ministry of Corporate Affairs, reported in June 2024, said that they had not found any financial fraud in the company, they informed about the lapses in corporate governance in the edtech giant.

Now, let’s see Zepto- In media briefings, Palicha, the CEO of Zepto, has often stated that 70% of Zepto’s dark stores are profitable. However, investors told one of the media outlets that this figure referred to only 338 stores that Zepto operated before the funding discussions began in April and not the new outlets that were opened in the subsequent months. According to Palicha, the network currently comprises over 750. According to a person working at Zepto, it would be fair to say that 60-70% of the 338 stores are contribution-positive or close to it, not accounting for cafe investments in stores and new store launches.

Palicha said the store push and new product categories would mark the next four months. When asked about ‘Is this $30 million (burn) going to sustain for a very long period?’ he gives the answer as no, adding that if full capex and working capital are removed, the cash burn mentioned above is an order of magnitude lower. However, industry insiders continued to contest this claim. By March 2025, the company plans to pause its expansion drive and return to the plans for achieving better unit economics, a challenge it first took up in April 2024. Industry executives caution that this transition may not be as straightforward as it appears.

Post-March, all the company need to do is stop launching stores. With improving in-store profitability, increasing mature customer profitability and better operating cost leverage, such as automation in our back-end mother hubs, Zepto will soon break even and regain the market’s licence to invest, Palicha said. As usual, this is easier said than done. The company will need to achieve multiple milestones simultaneously.

Hence, these types of opaque statements about the founder point to the direction of lack of transparency and clear path to profitability as witnessed with Byju.

Why so many high profile exits?

- After the resignation of auditor at Byju, board members of various investors, including GV Ravishankar of Peak XV partners, Russell Dreisenstock of Prosus, and Chan Zuckerberg’s Vivian Wu resigned on June 2023.

- Cherian Thomas, SVP for international business, quit in August 2023.

- Mrinal Mohit, Byju’s founding member, exited on September 2023.

- On October 2023, the Group CFO resigned within 6 months of joining.

- Anil Goel, Group CTO and President of Technology, resigned in November 2023.

These high-profile exits have shown that turbulent times are ahead for Byju.

A similar thing is now seen in the case of Zepto.

- Recently, Martin Dinesh Gomez, the Chief Human Resource Officer (CHRO) at Zepto, who joined Zepto less than a year ago, has resigned from his position and will be leaving the quick commerce startup soon, signaling turbulence at the quick commerce startup.

- Earlier in June 2024, Manik Oberoi, the former VP of Growth and Retention, left the company.

- Then, this was followed by the departure of Viral Jhaveri, the ex-Chief Business Officer and Chief Growth Officer.

- Ashish Shah, the former Senior Vice President of Finance, also left the company earlier this year.

These exits reflect the ongoing leadership changes at Zepto, which continues to navigate challenges in the competitive quick commerce space. The pattern follows a troubling pattern of senior departures across growth, business, and finance divisions, raising questions about stability at the high-growth company.

The ultimate question of survival.

Byju was a great teacher till the greed of the company did not take over. Then came a turning point, the ultimate boom came in 2020, thanks to the pandemic. As schools were shut, online learning was widely adopted, helping the established edtech capitalise on it in a big way. However, the turning point turned into a dead end after the pandemic was resolved. Byju began missing its step in a post-pandemic world as kids went back to school and logged out of online learning. Its revenues in FY21 dropped to ₹1,551.64 crore, with a loss of ₹2,702.14 crore, on a standalone basis.

Will Zepto also have a face a pre pandemic disaster? Zepto took the opportunity of quick online delivery when the lockdowns occurred in 2020 and everyone was grounded to their homes. Fast forward to 2024, will audience always be loyal to zepto?

The concept of online and quick delivery was first pivoted in the US, where people have a culture of placing orders on delivery apps. However, in India, the culture of purchasing groceries and more from online delivery apps is not very common. They can be fruitful in metros and mega towns, but as you move towns to smaller regions, people still have the habit of walking or driving to their grocery stores. Also, the congested places in small towns are a big block to the creation of dark stores in smaller regions, which is the foundational block of Zepto.

Therefore, as Byju is struggling to survive, will Zepto face a similar fate?

The bottom line.

Businesses built on shaky foundations and dishonest business methods are, by nature, brittle. The demise of businesses such as Byju’s points to a story of skewed incentives rather than merely bad business decisions. When those at the helm, founders, investors, and consultants, are insulated from the consequences of their actions, it creates a breeding ground for reckless choices.

Zepto, initially launched with the intent of growing, was justified. But this untamed desire to grow at any cost puts the company in question. Moreover, the unit economics of the business model, which is the basic block of the business, is in a doubtful situation, and then sooner or later, the collapse is on the way. Hope, we do not see another byju with the face of zepto!