From Buy Now Pay Later (BNPL) To Die Now See You Never, How ZestMoney Fell From 450 Million To 0?

ZestMoney, an Indian fintech startup, was once considered the poster boy for India’s Buy Now Pay Later (BNPL) market. It was valued at $445–$450 million at its peak. However, it’s almost been 1 year that the company has since shut down.

So what happened with ZestMoney that it went from $450M to $0?

December 2023, Chilly Evening winter- ZestMoney’s top leadership had an important town hall gathering.

In an unexpected revelation in a townhall meeting on December 5,2023, they stated that the fintech startup would stop operations by December 31. They told the staff that all lending activity will cease and recommended them to look for alternative career possibilities. Following the town hall meeting, employees, who tried to enquire about their December salaries were met with uncertainty from senior management, with no severance packages being offered.

That’s how the casual winter evening at ZestMoney converted into a spine chilly atmosphere for the employees, which was a once-hot fintech startup that garnered USD134 million in equity capital and had a peak valuation of USD 450 million. Several investors, including Naspers, Goldman Sachs, Omidyar, and PayU, stand to lose money on this venture.

May 2023- But all this doesn’t have its fire in the chilly winter, rather it all started with a ‘chingari’ in the hot summer.

The abrupt exit of Lizzie Chapman (the now-former CEO of ZestMoney), Priya Sharma (CFO & COO), and Ashish Anantharaman Ashish Anantharaman (CTO), on May 13, in a heartfelt letter to the employees, along with job cuts impacting approximately 100 employees then was a signal that some unrest is going in ZestMoney. In an e-mail response, ZestMoney co-founder Lizzie Chapman said that all impacted employees have received two months of severance pay apart from six months of medical insurance for self and family and access to counselling.

During the May 16 town hall meeting, ZestMoney also introduced its new leadership. Mohit Chhajer, VP of Finance, Mandar Satpute, Chief Banking Officer, and Abhishek Sharma, SVP of Growth, took over the leadership. Employees were tensed but put their faith in this new direction.

March 2023- Wait, not winter, not summer; the hints of ZestMoney losing its zing can be traced back to the 2023 Spring.

In late 2022, desperate for survival funds, ZestMoney approached PhonePe for a buyout. And everything was progressing quite smoothly. As part of the agreement, PhonePe funded ZestMoney USD 18 million and received exclusive rights to negotiate a merger and acquisition deal. Due to the indebted nature under which the conversations began, ZestMoney opened its whole technological stack and initiated thorough integration with PhonePe. At least inside ZestMoney, there were no questions about PhonePe’s intentions, or any worry that the giant may back out of the deal.

However, it came as a shock when news surfaced in April 2023 that mobile payments giant PhonePe had pulled out of an agreement to purchase the BNPL start-up.

But Phone Pe needed ZestMoney as much as the fintech poster boy needed it.

For PhonePe, this was the perfect match. Paytm, one of its main competitors, has been writing a recovery story centred on lending, while ZestMoney has a large BPNL loan portfolio. For each fintech startup, lending is the ultimate frontier since it is where the real revenues lie.

PhonePe needed ZestMoney just as much as the fintech did. Despite offering a variety of financial products and services to its consumers, like insurance and investments, PhonePe’s payments processing produced approximately 99% of its income in FY22. In other words, despite having a large user base of about 200 million, its ancillary revenues have not increased significantly. As start-ups face increased pressure to show profitability in the midst of a financing winter, payment processing alone cannot provide PhonePe with the growth it seeked at a valuation of USD 10 Bn-USD 12 Bn, as its investors expect during the present funding round.

Then, why the giant PhonePe said No to ZestMoney at the end?

First- The jumping game of valuation, which never proved its justification.

The USD 440 million valuation that ZestMoney commanded in a big investment round in June 2022 constituted a substantial revenue multiple over earnings. However, it quickly proved difficult to justify this valuation. Even a substantially lower valuation, an asking price of roughly USD 300 million, failed to impress PhonePe within handful of months of negotiations. Even with USD 4 million emergency injection of funds in July 2023, could not arrest this downward spiral, and ZestMoney’s worth fell to barely USD 8 million.

Second- The greed; Growth at all cost- even if the cost costed the survival of the company.

An ounce of prudence is worth a pound of gold, goes an old saying. Attempting to grow at break neck speed, unfortunately often results in the neck being actually broken.

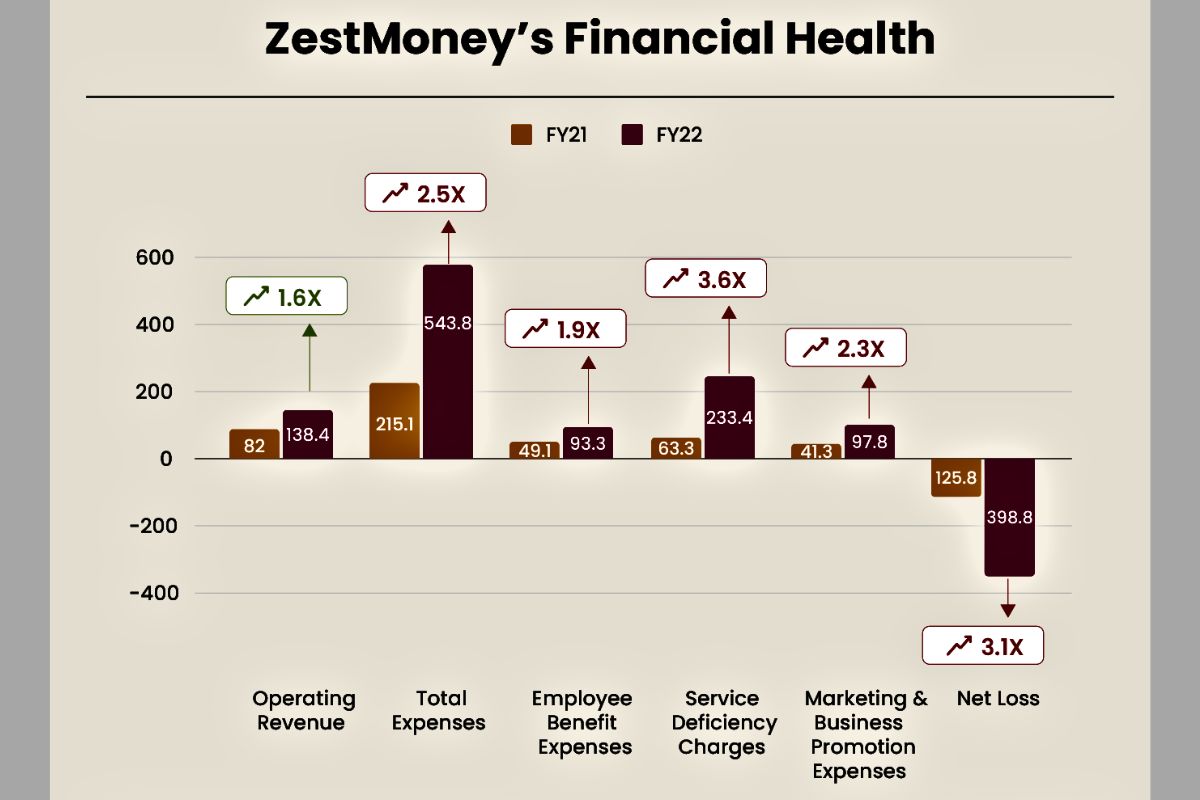

ZestMoney embraced a growth-at-all-costs strategy. At its peak, the company was worth roughly USD 450 million. It had more than 11 million customers and a network of over 75,000 merchants, both offline and online. ZestMoney has disbursed more than USD 1 Bn. This resulted in huge losses and large NPAs (non-performing assets), forcing the firm to seek debt finance in the middle of 2022. This attempt forced ZestMoney to walk into the doors of PhonePe a few months later.

Third- Imbalance in the balance sheet.

While negotiations with ZestMoney began for a deal of USD 200 million-USD 300 million, PhonePe discovered significant delinquencies in ZestMoney’s records. NPAs of more than 10% were found to be greater than expected. ZestMoney’s yearly losses of INR400 crore were about one-fifth of PhonePe’s losses and less than one-twelfth of its revenue. By March 2023, after looking over ZestMoney’s books, PhonePe was unable to even offer USD 90 million for the deal. The negotiations fell down, and ZestMoney investors scrambled to raise a fresh round to keep the firm going.

Fourth- Subpar collection system.

Apart from the deficiencies in the balance sheet, PhonePe found ZestMoney’s collection processes, infrastructure, and network to be inadequate for the type of loan book it has built. Giving out loans is easy, but collecting the money is difficult. Even huge NBFCs, like Bajaj Finance and Mahindra Finance, have suffered with this.

Ketharaman Swaminathan, the Founder & CEO at GTM360 Marketing Solutions, beautifully twitted this situation from historical examples explaining how Andhra Bank with credit card in 1990s; Citi and Barclays in 2000s; Fullerton in 2010s; ZestMoney in 2020s joins a long line of lenders who learned the hard way that it’s easy to lend but hard to recover loans in a market like India where loan recovery laws are pro borrower.

PhonePe has been quickly expanding its top line while minimising its losses, and any acquisition comparable to ZestMoney will bring it back deep into the red, something no start-up can afford right now, despite the massive capital commitments.

Fifth- The final Blow- the Regulatory Crackdown.

For far too long, BNPLs in India functioned without the RBI’s direct regulatory control. This changed with the adoption of digital lending rules in December 2022, which designated BNPLs as Lending Service Providers (LSPs) capable of collaborating with regulated banks and NBFCs to resell packaged loans.

In a new set of guidelines issued in June 2023, the RBI also examined the lending arrangements between digital lenders (including BNPLs) and NBFCs, with an emphasis on first-loss default guarantees (FLDGs) offered by digital lenders to cover prospective non-performing assets.

In November 2023, the RBI issued an instruction to banks and non-banking financial companies (NBFCs) to raise the risk weight on unsecured personal loans from 100% to 125%. Additionally, the RBI imposed a 25% increase in the risk weight for banks’ exposure to NBFCs. Risk weights are the capital reserves that financial institutions, like NBFCs and banks, must hold against unsecured loans. This increase in risk weights raises the cost of capital for NBFCs, which is expected to be passed on to lenders, including digital fintech businesses.

The RBI’s new risk weight standards were expected to increase NBFCs’ funding costs by 25-70 basis points. As a result, these NBFCs were expected to hike their charges, potentially increasing the cost of funding for fintech startups by up to 100 basis points. Going by an expert opinion, “Digital loans were expected to become more expensive for the consumers and the underwriting norms will get stricter,” said Rohan Lakhaiyar, partner at Grant Thornton Bharat. “The improved screening of borrowers’ credit worthiness means less digital loans will be sanctioned by fintech businesses in the near future,” he noted.

The already high delinquency rates among its customers along with this led to a substantial liability owed to its NBFC partners under First Loss Default Guarantee (FLDG) agreements. FLDGs serve as safety nets, either in cash or bank guarantees, given by digital lenders to cover NPAs for their lending partners, which include NBFCs and banks. Online lenders provided guarantees ranging from 20% to 100% to these partners to offset risks from failed loans, with no regulatory restrictions and essentially absorbing all liabilities. ZestMoney had many FLDG agreements with its partner NBFCs.

However, the RBI intended to change this. In new rules announced on June 8, 2023, the apex bank stated that defaulted guarantees provided by digital lenders to regulated businesses should not exceed 5% of the total loan portfolio value. ZestMoney had opted to discontinue all FLDG arrangements with lending partners prior to this news and instead pursue direct lending ties with all of its lenders.

You may think that the attempt was in sync with RBI’s mandate. The answer is NO. This shift to direct lending was not in response to the RBI mandate, but rather because, by the end of FY23, ZestMoney’s loan portfolio, which comprised loans sold both online (e-commerce sites and online merchants) and offline, began showing NPAs significantly above market standards. ZestMoney’s online NPAs were already in the red, reaching 10% in the fourth reporting quarter of FY23, while offline loan NPAs increased to roughly 16%-18%.

Throughout the PhonePe deal talks, ZestMoney maintained FLDGs with all of its lending partners. Faced with rising default rates, the fintech poster boy decided to liquidate these guarantees and restructure all financing arrangements as direct partnerships. To ease this deal, ZestMoney bore a significant obligation of INR 400 crore to its lenders for the current default guarantees. This payment coincided with the ongoing PhonePe deal discussion.

One may say that regulatory crackdown by RBI may have burdened the BNPL startup. However, ZestMoney incurred INR233.48 crore in “service deficiency charges” (SDCs) in FY22, according to company financial papers submitted with the Registrar of Companies. This suggests that the firm has already incurred a huge financial burden for its FLDG arrangements in FY22, up from INR63.31 crore in FY21.

The rise of BNPL and Fintech startups In India.

BNPL services have exploded in India over the last few years, with various fintech startups fighting for our attention. These include embedded fintech partners on e-commerce giants like Amazon and Flipkart, and several fintech startups competing to be our checkout partner on food-delivery platforms like Swiggy and Zomato.

Despite the fact that India has abysmally low credit penetration, given the prevalence of BNPL fintechs, it is quite improbable that you have not used their services at least once – intentionally or unwittingly. In reality, there have been countless cases where people signed up for BNPL credit without understanding it. Some well-known payment applications have been accused of crediting loans to consumers’ prepaid wallets without their explicit permission.

While you may be required to provide your PAN card to sign up for a BNPL service, depending on the issuing company’s business strategy and know-your-customer (KYC) policies, many may merely ask for your phone number. According to 2022 estimates, India has 25 million BNPL customers, while the segment’s biggest providers, Paytm Postpaid and Amazon Pay Later, both have more than three million. According to data from credit information business TransUnion CIBIL, BNPL in 2022 accounted for around 15% of all unsecured consumer loans, which is a significant portion.

Founded in 2015 with USD 2 million in venture investment from investors like Ribbit Capital and Omidyar, ZestMoney’s business model focused on using machine learning and artificial intelligence (AI) to underwrite consumer loans for e-commerce. It served as a digital distributor for financial institutions with the goal of giving online buyers access to EMIs. Targeting new-to-credit consumers in India, ZestMoney swiftly rose to prominence, competing with industry titan Bajaj Finserve and moving from online to offline marketplaces. Notably, ZestMoney’s shutdown teaches important lessons for the developing digital lending sector, which has spiked USD350 Bn in 2023.

The reality of fintech startups.

Fintech companies frequently claim that they have extended the reach of formal credit to a large number of new customers who are not served by banks. According to them, they have also helped increase consumer consumption, making the economy more robust throughout the pandemic.

However, according to a 2022 report on BNPL by Kotak Securities, which is based on data collected from TransUnion CIBIL, BNPL has a smaller percentage of new credit consumers. Furthermore, typical BNPL customers are not significantly different from borrowers of other unsecured retail loans, while the former is more likely to include subprime customers than the latter. Contrary to common opinion, the age range of customers is not very diverse. The proportion of borrowers under the age of 25 was 26% for BNPL and 19% for non-BNPL credit, which included durable loans, personal loans, and credit cards.

Also, according to ndtvprofit.com, Kotak Institutional Equities’ report on BNPL in June 2022 stated that BNPL could become a competitor to credit card companies, but it was not expected to be a disruptor. This raises a couple of questions:

Do venture capital-backed BNPL services have a long-term future in India?

Was ZestMoney’s downfall largely the result of a funding crunch, regulatory issues by RBI, or unmanageable NPAs?

Answering the future of BNPL services in India, Ketharaman Swaminathan writes that People below a certain age who are witnessing their first boom-bust cycle in this space often wonder why unsecured lending, which comprises credit card and BNPL, can’t be a “steady business”. He goes on to say that, based on his experience over the last three decades, unsecured lending would always go through boom-bust cycles, particularly in a market like India where per capita income is low and fewer than 5% of the population is eligible for unsecured loans. Unless the underlying structural challenges of demography are addressed, unsecured lending will continue to be rough.

If we connect these dots with ZestMoney, similar nodes can be found interconnecting with each other. As ZestMoney moved to new leadership, it had a big challenge; a delinquency rate that had risen into the double digits (about 16%-18%). This needed an urgent shift in effort to improve collecting. Banking specialists argued that such attempts may be in in vain. The reason for this was that most consumers who defaulted on BNPL services like ZestMoney had relatively low monthly EMIs ranging from INR3,000 to INR5,000, with some paying even less.

According to Piyush Kumar, regional sales manager at Poonawalla Fincorp, “the cost of recovering these small EMI payments through an on-ground collection team is so high that it often makes more financial sense for the finance company to write it off and classify it as an NPA, rather than incur a greater expense for recovery.” Collections were quite weak, making recovery attempts more difficult.

This was primarily due to the customer’s severe financial situation. Despite efforts to promote payments, many people were unable to pay. As a result, some NBFCs’ loan portfolios began to bleed. The RBI took note of this alarming trend and implemented new capital requirement procedures in November,” he noted. Hence, the doubt of BNPL future in India makes sense.

But why BNPL recovery is critical?

For people with a limited income, the BNPL (buy now, pay later) model is handy. The simplicity of using BNPL may lead to rash purchases and difficult-to-manage debts. A survey in India discovered that 60% of BNPL users accepted to spending more than they could afford. These BNPL firms give money without any security, so if someone is unable to repay the loan, they have no assets to recover it.

Now let’s try to answer the second question that raises doubt about the unmanageable NPAs. It was observed that significant portion of the growth to fintech companies were those especially targeting younger demographics and individuals new to credit. This resulted to a surge in the origination of low ticket-size loans, thereby limiting the average ticket size of NBFC loans. Loans below INR 1 lakh made up over 85% of loan originations by volume in FY23. The majority share of origination volume was for loans below INR 50,000, which saw a more than two-fold increase in value in fiscals ending March 2023. This trend could have contributed to challenges in the segment.

It was concluded that though such low ticket-size loans played a role in integrating new-to-credit consumers into the formal economy, they also carried inherent risks. It was found that about 32% of loan accounts with ticket sizes under INR 10,000 in FY23 were contributed by tier four towns, facilitated by fintech companies tapping into previously unexplored markets.

But what forced RBI to intervene?

Children, or the young folks, as described earlier, in India are not taught how to utilise credit, so in the pursuit of pleasing others and concealing their fears, they engage in impulsive purchases and ultimately default on loans, degrading their credit rating and establishing poor financial habits.

The suicide of a techie in October 2022 in Tamil Nadu, due to alleged reception of threats from loan app operators, and the suicide of a couple just a month ago in Rajamahendravarman Anandanagar in Andhra Pradesh’s East Godavari district, due to incessant harassment by loan recovery agents, raised the eyebrows of the apex bank RBI. Bankers observed early signs of trouble brewing within the unsecured lending sector as a whole, indicating potential risks on the horizon. And the regulatory measures undoubtedly slowed the mind-boggling rate at which the BNPL industry has been expanded.

Considering an expert opinion, Anurag Jain, founder and executive director of KredX, argued “BNPL was originally intended for small, unsecured consumer loans like white goods, mobile phones, and electronics. The fundamental difficulty was from the credit underwriting process, where decision-making algorithms and processes may have been insufficient in effectively assessing customer risk, resulting in an unexpectedly high default rate.”

Answering about the impact of regulatory crackdown by the apex bank of the nation, Mr Jain further described the RBI’s enhanced capital requirement ratios as a watershed moment for financial institutions that engage in unsecured personal loans. “With lenders becoming cautious ZestMoney faced significant hurdles. Hence, the company lacks the drive and spirit to keep going without new business for multiple quarters, which eventually pushed the new management team to take the final decision on the chilly winter oof December 5, 2023.

Is it just a coincidence that BNPL poster boy fall? Is PhonePe-ZestMoney failure is a single event signalling the dismal state of BNPL sector?

The answer is a NO. PhonePe-ZestMoney is the second high-profile fintech merger to fall through. This corresponded with a funding crunch that has begun to materialise in India’s startup ecosystem. In 2022, Prosus withdrew from the USD4.7 Bn acquisition of payments gateway business Billdesk through its Indian subsidiary PayU.

The bottom note.

What happened to ZestMoney may be a sign of danger in the bigger BNPL fintech space. Stricter RBI guidelines restricting the default guarantee to lending partners, unstable default rates, a massive increase in marketing expenditures, and declining interest from venture capital (VC) investors all make the future for BNPL players uncertain.

For some years, RBI, has been concerned about the zooming growth of personal loans through such platforms. The apex bank has advised banks and NBFCs to be more careful while lending to digital platforms. Furthermore, civil rights organisations have pushed for the elimination of predatory financing and harassment in recovery methods.

The market is overflowing with digital lending platforms, which may be why the RBI opted to enhance risk weights in order to avert a long-term disaster. Fintech companies are increasingly discovering that restrictions are the norm rather than the exception in this field. In some respects, companies are acknowledging that merely turning on the digital lending tap may not be sufficient. In that way, ZestMoney can be studied as a cautionary story for the fintech ecosystem.