Controversy of Rs 2,331 crore Minimum Balance Charges by Public Sector Banks in India: A Deep Dive

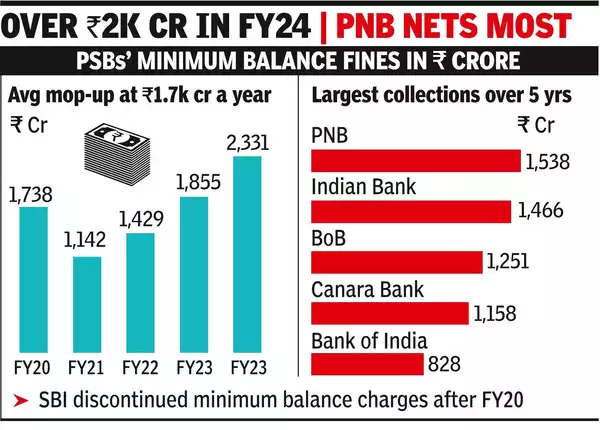

Public sector banks have been the backbone of India’s banking system for a very long time. However, all that has come under severe review with recent revelations about these institutions. Eleven public sector banks have collectively charged Rs 2,331 crore for non-maintenance of minimum balance in FY24. It showed a spike of 25.63% from the last fiscal year. This article deals with details, implications, and public reactions post such levying practices, adding to an analysis on the same.

Overview of the Charges

In FY24, 11 public sector banks penalized their account holders Rs 2,331 crore for not maintaining a minimum balance in their accounts. Leading this list is Punjab National Bank (PNB), which mopped up Rs 633.4 crore, followed by Bank of Baroda (Rs 386.51 crore) and Indian Bank (Rs 369.16 crore). If anything, this indicates that such charges are increasing, which is a concern for the burden the penalties put on customers, especially those in lower-income brackets, where they are hurt most.

RBI Guidelines and Compliance for banks

The RBI has laid down clear guidelines to maintain a minimum balance. Banks are supposed to advise their customers regarding the minimum balance requirement while opening an account with the bank, and any revision thereof from time to time. In addition, the banks need to ensure that such charges would not lead to a negative balance.

But the way penalties have been piling up would suggest that banks are more interested in earning money rather than serving the customer. The State Bank of India (SBI), the largest public sector bank in India, stopped charging a penalty for not maintaining the minimum balance in FY20, but other banks have not followed suit.

Geographical and Demographic Disparities

Banks from the public sector have different threshold configuration for low balance requirements across geography and customer segmentation. However, this approach is not scalable and may lead to accretion which may be more discomforting to the rural and weaker sections of the customers. Therefore the disparity in charges, the non-standardization of these changes, and the lack of transparency in the banking system are being put on the table for the first time.

Public Reaction and Criticism

The news of the enormous penalty imposed on account holders not being able to keep the minimum balance in their bank has caused the public to be outraged. Complaint clients say that these fees are unnecessary, particularly in a country that is on the road to financial inclusion as the case is in India. However, the bulk collected by the banks hints that a relatively large number of account holders are not having the balance they required, which points out to the fact that there is a systemic problem rather than individual ones.

The trade-offs that come in the form of charges are purely one-sided and actually, it is the poor people who are the most affected of all. These people demand their banks to have better and more forgiving policy requirements, as well as to be more attentive in relaying the correct information so that people should not become overcharged.

The Role of Financial Literacy

The low financial literacy rate is one of the most critical factors that led to the problem among the part of the population. More often than not, the people have only a hazy idea of what the results of non-maintenance of the minimum balance might be. Therefore, the banks must put in more money in training the clients and endorsing the requirements and the events that can follow if the customers do not comply with them which will result in the clients being more informed.

Alternatives and Solutions

To manage the problem, banks have the following options. They might:

Lower Minimum Balance Requirements: Instead of the mergers, it is possible to raise the threshold for those low, which means that people can frequently avoid being charged a violation fee. You get rewarded for your correct actions, dear kiddo, the more you correct the better the action, the more you get.

Waiving Charges for Certain Segments: Instead of one-argued solution, the banks can choose two of the two paths for the weak group such as Giving away Fees and Negative Taxation on pump oil station oil.

Better Communication: Financial relationship managers can use better communication strategies to ensure that the customers are aware of their account demands as well as the implications of non-compliance.

Financial Inclusion Initiatives: the emphasis should be on the financial inclusion programs by the banks, so that more people are brought into the regular banking system and also the transformation of financially burdened sections.

One of the startling bank activities to make the non-maintenance of minimum balance mandatory and penalize the defaulting customers with a total of Rs 2,331 crores has revealed several issues in the public sector banks.

In the meantime beyond all the drastic penalties these situations witness, the customer-friendly conclusion remains as one of the key issues. By adopting strategies of behavioral finance, increasing education, and levelling of profit-making banks with other industries, the banks have the opportunity to provide better customer service as well as reducing the financial constraints of the rest of the economy.