Beware Of Investing In Loss-Making Ola Electric IPO Likely To Launch Next Week; Founder Is Selling Most Of His Shares

Ola Electric IPO is a red flag. There are multiple product faults and no profit pathway. Investors Should Proceed With Caution while Investing.

Ola Electric is launching the anchor book for its much-awaited Ola Electric IPO on August 1. It is expected to be available for public subscription from August 2 to August 6. August 3 and August 4 are occurring on a weekend.

The firm’s listing, which is expected to be the first-ever Indian electric two-wheeler to enter Dalal Street, is to occur on August 9, according to the proposed timeline, according to sources. Ola Electric refused to provide an official response.

Moneycontrol reported on July 24 that Ola Electric is seeking to raise approximately USD 740 million (Rs 7,250 crore) through a fresh issue and an OFS (offer for sale) combination. The company is aiming for a post-money valuation of $4 billion to $4.25 billion. It is worth noting here that this is a 16-20% decreased valuation from its last funding round, highlighting the inflated numbers of the company.

TVS Motors, Bajaj Auto, and Ather Energy are the top companies the organization directly competes with.

On December 22, 2023, Ola Electric submitted its draft red herring prospectus (DRHP) to the market regulator SEBI. It proposed to raise up to ₹5,500 crore through a fresh equity issue, with a target valuation of USD 5 billion. Furthermore, the organization intends to execute an offer for sale (OFS) of 95.19 million equity shares, each containing a nominal value of ₹10.

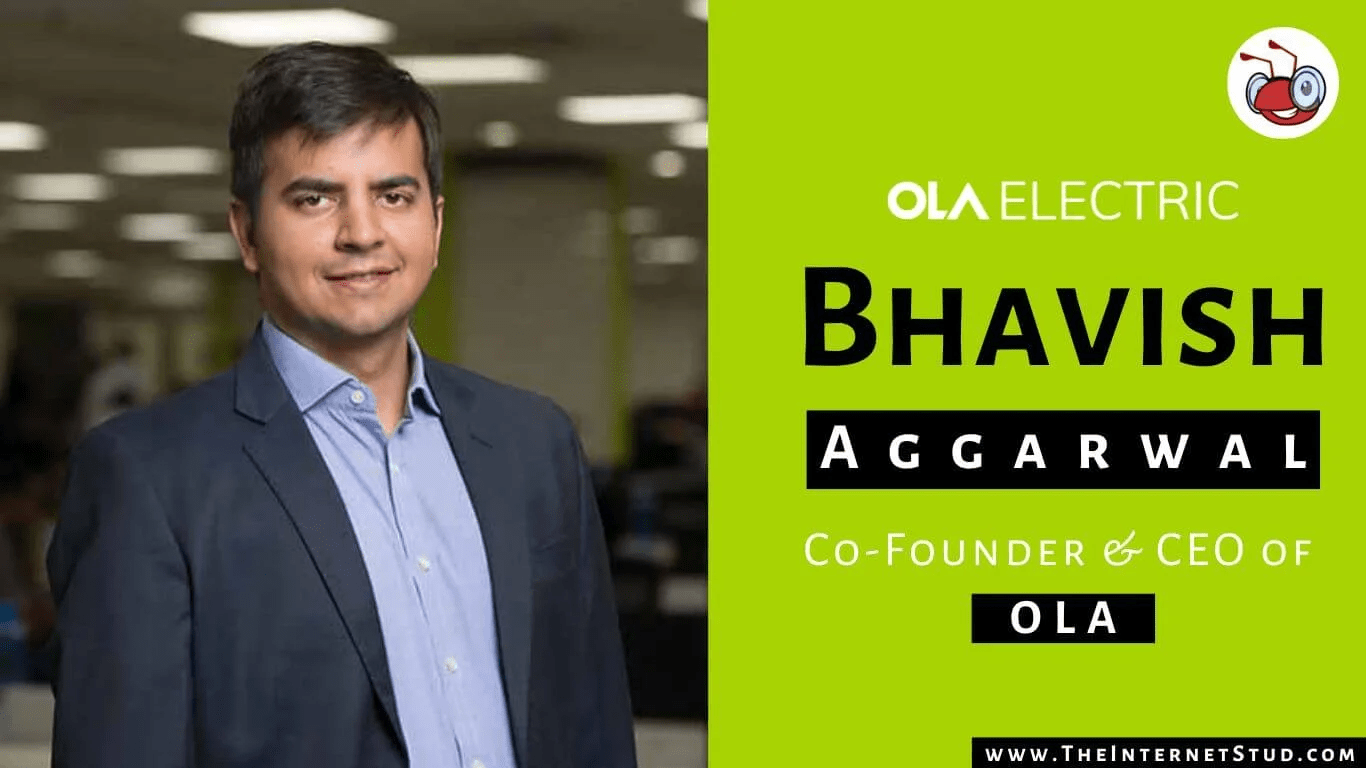

Bhavish Aggarwal, the founder and CEO, plans to sell the greatest portion, which is 47.3 million shares, which is half of the total number of shares available for sale.

The funds from the Ola Electric IPO will be allocated for capital expenditure, debt repayment, and research and development (R&D), as per the DRHP. To be more precise, approximately Rs 1,226 crore will be allocated for capex, Rs 800 crore for debt repayment, Rs 1,600 crore for R&D, and Rs 350 crore for inorganic growth.

Loss-Making Company, With No Path To Profitability

In December 2022, Ola Electric reduced its sales targets for 2023-2025 by more than 50% and postponed its goal to achieve profitability by one year. This was the consequence of the government’s reduction in incentives, which led to an increase in the price of e-scooters.

Although revenue from operations increased by over sevenfold, standing at ₹2,631 crore, the total loss for the fiscal year ending March 2023 increased to ₹14.72 billion ($176.14 million).

The company experienced a net loss of ₹267 crore during the first quarter of FY24, with an operating revenue of ₹1,243 crore.

Ola Electric’s financial situation has been nothing short of catastrophic in recent years:

FY 2023: A loss of ₹1,472.08 crore

FY 2022: A loss of ₹1,292 crore

FY 2021: A loss of ₹1,174 crore

FY 2020: A loss of ₹890 crore

FY 2019: A loss of ₹625 crore

The company’s sustainability and growth prospects are cast in doubt by these figures, exhibiting a pattern of escalating losses.

For the fiscal year 2023, ANI Technologies, the parent company of the Ola brand, disclosed a consolidated net loss of ₹772.25 crore. Their financial performance is summarized below:

FY 2023: A loss of ₹772.25 crore

FY 2022: A loss of ₹1,108 crore

FY 2021: A loss of ₹924 crore

FY 2020: A loss of ₹659 crore

FY 2019: A loss of ₹556 crore

This astronomical loss is part of a worrying trend.

Flawed Business Model

While historically, loss-making numbers are a sign of worry, the bigger concern is that there is no clear path to profitability. Ola Electric created a lot of buzz in the market for its “state-of-the-art” electric scooters but failed to prove itself due to flawed designs, which will be covered later in the article.

Ola Cabs, the ride-hailing arm of the parent company, in all likelihood, will not be able to make profits as the business model is flawed. The leadership realized this pretty early on, and hence, Ola Electric was started. However, it does not seem promising either.

Failing to understand the product-market fit highlights the incompetence of the leadership.

The GDP per capita of the United States is USD 70,000, that of China is USD 12,000, and that of India is approximately USD 2,200 (equivalent to INR 1.8 lakh per year). Ask yourself: How many cab journeys could a person earning 1.8 lakh annually afford? Most of all once a month, on a good day.

Nevertheless, Uber and Ola’s heavy discounts allowed people in the lower income bracket to use cab transportation services on a weekly basis. The cost came out almost equal to that of an auto-rickshaw.

These companies generated buzz as a result of this phenomenon, which was termed “market disruption.” The reality is that the “disruption” was merely the burning of currency in the millions. Uber and Ola have collectively consumed more than INR 30,000 crores, according to data.

Cash-burning became increasingly challenging as the funding environment became more stringent, and investors began to demand profits. Subsequently, discounts diminished, prompting individuals to return to public transportation and rickshaws in lieu of taxis.

In conclusion, the service is not experiencing difficulties due to the apathy of the companies; rather, it is a result of the business model’s inability to expand to this extent. It functions exceptionally well as a niche service for the affluent class, which can afford the actual cost of an air-conditioned taxi without hesitation (or perhaps with some).

This service was never truly “for everyone.” It appeared to be the case because the money from venture capitalists was inflowing, enabling these companies to burn cash in profusion in the name of “making business” and “acquiring users.”

Startup enthusiasts frequently assert that these investments are made with the “future” in mind. The conviction that these “habit-forming” services will eventually become profitable as India’s discretionary spending increases. In essence, the business paradigm is predicated on a future scenario that may never materialize. With the corporation being at odds, the path to profitability is actually a significant probability.

At what income level would an average individual be prepared to pay a premium for such amenities? A per capita income of USD 6,000 (INR 4,80,000 per year). Currently, this is the case. This figure would rise in the future, with inflation in consideration.

The GDP per capita of a nation is calculated by dividing its GDP by its population. Assuming a constant population, India’s GDP would need to attain nearly USD 10 trillion in order to achieve a GDP per capita of USD 6,000. India has the potential to become a $5 trillion economy by 2024-25 or 2028-29, as per Prime Minister Modi. Even if that were to occur, the GDP per capita, a more precise metric, would remain insufficient for the average individual to utilize these services.

Some contend that the national GDP per capita is an overly broad metric and recommend that the focus be on the GDP per capita of metropolitan cities such as Delhi, Mumbai, Pune, Bangalore, Chennai, Hyderabad, and Kolkata.

With regard to Delhi, the GDP per capita exceeds USD 5,000. However, is it possible for a metropolitan city to serve as an accurate benchmark? What is the number of cities in India that are similar to this? A maximum of four, with a combined population of less than 100 million.

In what way does this substantiate the investment thesis of “capturing a market of 1.3 billion people”? How does it make sense to account for the cumulative losses of over USD 4 billion that Uber and Ola have suffered? Furthermore, why is Ola operating in 160 cities if the strategy has always been to operate in metro cities?

Wouldn’t Ola Autos be a more suitable option for India? The operation of automobiles on such a large scale was never logical and remains so. Uber and Ola may be promoting automobiles at an unprecedented rate in the next five years. This change is comprehensible.

Top Reasons To Not Invest In Ola Electric IPO

1. Founder and Early Investors Offloading Maximum Shares

The substantial quantity of shares that promoter Bhavish Aggarwal is selling in the OFS is a noteworthy feature of the Ola IPO. He intends to dispose of 4.73 crore equity shares through the initial public offering.

Given that Aggarwal, the primary promoter with the largest shareholding, is selling nearly 50% of the shares in the OFS, concerns regarding his confidence in the future prospects of Ola Electric have arisen.

Aggarwal owned a 36.94% stake in Ola Electric prior to the Ola IPO listing, while ANI Technologies and Indus Trust held 4.35% and 3.85%, respectively.

SVF II Ostrich (21.98%), Alpha Wave Ventures II (3.49%), Internet Fund III (6.03%), and MacRitchie Investments (1.25%) are among the substantial shareholders that have reduced their stakes in Ola Electric following the IPO.

If the investors are offloading their shares, what does it signify if not a complete loss of trust in a failing business? Which founder would be willing to give up such a large stake in his own company, unless it is a company that he no longer believes is worth investments.

Ola Electric brand and buzz would lure many first-time investors to invest, however, it is a very big mistake to invest in a venture which has been abandoned by its promoters. Hence, immediate caution must be exercised.

2. Product Faults

Numerous reports of defects and quality issues have afflicted the EV market, particularly Ola Electric. These encompass a wide spectrum of issues, including battery malfunctions and general vehicle reliability issues. Consumer trust and the brand’s reputation are undermined by such matters.

Ola Electric asserted that it had sold more than 100,000 scooters on its inaugural day, prior to the product’s availability for delivery. The company’s commitment to deliver the scooters within a month was not fulfilled, as they consistently postponed deliveries. They attributed this to the semiconductor chip shortage; however, if production was not prepared, why did they pledge a one-month delivery timeline?

Images of a blue Ola S1 Pro with its front tire detached following a head-on collision in Maharashtra were circulated in April, which prompted apprehension among Ola’s suppliers. Under the challenging conditions of India, the front fork limb of the S1 Pro malfunctioned.

In order to provide a smooth ride and navigate difficult terrain, the suspension unit is essential in two-wheelers. The suspension is connected to the wheel by Ola’s front fork arm, which is constructed from high-pressure aluminum die-casting and is cantilevered, with support provided solely on one side. This design is distinctive in the two-wheeler market of India.

In some cases, the rider abruptly applied the brakes, resulting in the arm breaking. It became increasingly apparent that the scooter was intended for European roadways that were free of traffic and were smooth, and that it was significantly unsafe for the conditions found in India as more incidents occurred.

The Ola S1 Pro’s design is influenced by the Appscooter, an electric vehicle manufactured by Etergo in the Netherlands. While it is permissible to draw inspiration, Ola neglected to modify the design to accommodate Indian conditions.

Ola had less than 50,000 scooters on the road when the initial incident was reported on social media. The company declined to redesign the component, which would have necessitated substantial modifications, despite the opportunity to resolve the issue. Nevertheless, they persisted in augmenting their produce.

“This would have allowed a responsible original equipment manufacturer (OEM) to gradually resume production, review processes, address issues, and slow down,” stated a source.

Additionally, there were reports of the scooter abruptly transitioning to reverse mode, which resulted in numerous accidents. Ola did not acknowledge the issue or proclaim a recall to resolve the severe problems in the software.

The majority of mechanical or engineering errors that brands make are rectified through a recall mechanism. This demonstrates the brand’s dedication to passenger safety, even at the expense of its own reputation. The brand Ola Electric appears to prioritize the preservation of its reputation as a disruptive and innovative scooter manufacturer over the prevention of passenger injuries.

3. Rising Competition from Other OEMs

Ola Electric reported that the S1 Pro model had a driving range of 195 km, while the S1 Air had a range of 151 km. Nevertheless, the actual range is approximately 40% less (130 km for the S1 Pro and 90-100 km for the S1 Air) and further decreases with a passenger.

Ola has been accused of deceiving consumers by displaying the certified range, which undergoes laboratory testing. The conditions of Indian roads substantially diminish this range.

In contrast, Ola Electric’s competitors, such as Ather and TVS, provide information on the exact range. For example, TVS discloses a genuine range of 100 km for its electric scooter.

Ola Electric achieved a huge market share in the two-wheeler EV segment through big discounts. Nevertheless, the company is under pressure due to the entry of established competitors such as Bajaj and TVS and fundamental issues with its products.

4. Founder’s Involvement in Multiple Businesses Raises Concerns

The DRHP emphasizes that Ola Electric’s originator, Bhavish Aggarwal, has priorities on numerous other businesses.

The Chairman and Managing Director of Ola Electric, as well as his involvement in Krutrim SI Designs Private Limited and ANI Technologies Private Limited, raise concerns about Aggarwal’s capacity to allocate an adequate amount of time and effort to Ola Electric.

Moreover, Aggarwal’s affiliation with Tork Motors Private Limited, a competitor in the same industry, introduces the possibility of conflicts of interest that could have a detrimental effect on Ola Electric’s operations.

The importance of this point can be seen in the numerous news that Ola Electric’s two-wheelers have garnered regarding fire incidents, service-related issues, and much more, as well as the lack of accountability from Bhavish Aggarwal.

5. Stagnating EV Volume

Over the past three months, the electric two-wheeler market in India has experienced a stagnant volume. In May, there was a 27% decrease in the number of high-speed electric two-wheelers registered in comparison to the same period last year. This decline is the result of a surge in pre-purchases that was prompted by the government’s decision to substantially reduce FAME-II subsidies for electric two-wheelers beginning June 1, 2023. Previously, these subsidies had reduced prices.

As a transitional policy to bridge the gap between the end of FAME-II (on March 31, 2024) and the forthcoming implementation of FAME-III, the government has further reduced subsidies since April.

With a 48% market share in May, Ola Electric was the dominant player. However, the percentage of electric vehicles (EVs) in the aggregate two-wheeler market remained consistent with the previous year, at 5%.

Investors are becoming more apprehensive about the potential growth drivers for electric two-wheeler ventures. An anonymous investor who was involved in an IPO stated, “We are in search of the next growth catalyst in the e-two-wheeler market.” The recent stagnation in volumes has redirected the attention of EV companies to the efficient use of capital and profitability.

The investor further stated that the quantity of subsidies for e-two-wheelers is expected to decrease, which will make these factors even more important in assessing the sustainability of these businesses.

The electric scooter market is becoming increasingly competitive as established competitors such as Bajaj Auto and TVS Motors increase their market shares to 19% and 12%, respectively, in FY24.

6. Closed international segment, on the pretext of focusing on domestic market

Ola Cabs has discontinued its international operations in the United Kingdom, New Zealand, and Australia. The company attributed the reason for its decision to concentrate on the India business to its rapid growth.

However, these international markets pose high growth for both EV and usual cab hailing. The high disposable income allows people to take cabs for commuting more easily than Indians.

This highlights that there exists a much bigger problem. There is lack of vision and implementation. If the businesses were shut down to “focus on the domestic market”, why hasn’t the Indian arm seen any profitability yet? Or any path to profitability?

Why is Bhavish Agarwal offloading his shares?

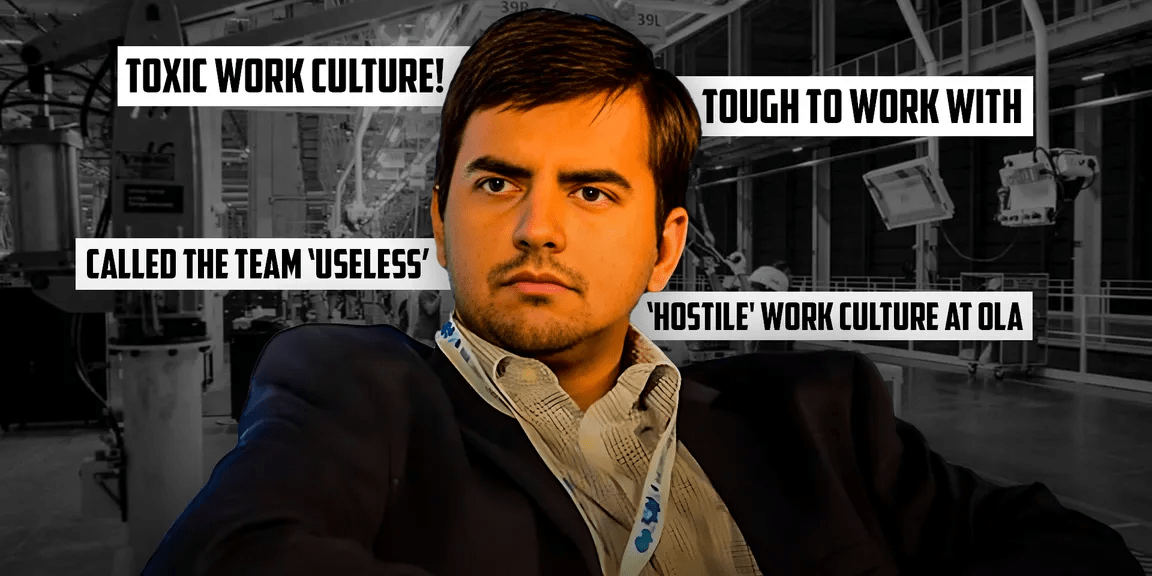

7. High Attrition Rate and Toxic Work Culture

The DRHP indicates a concerning attrition rate of 42.06% for the seven-month period ending October 31, 2023, and 47.48% for Fiscal 2023. The company had let go 200 employees from a variety of departments in January of the previous year.

Ola Electric is in the process of laying off approximately 400-500 employees as founder Bhavish Aggarwal devotes his attention to the management of operating costs in anticipation of the company’s impending IPO.

Karthik Gupta, the Chief Financial Officer (CFO) of Ola Cabs’ parent company, resigned on May 16, a mere seven months into his position. This was preceded by the departure of Ola Cabs’ CEO, Hemant Bakshi, who departed after only four months, indicating the possibility of internal challenges.

A spokesperson for Ola Cabs responded to inquiries regarding the layoffs by stating, “We conduct restructuring exercises on an ongoing basis to enhance efficiency, and there are positions that are currently redundant. We will continue to recruit new personnel in engineering and design, including senior talent in our primary areas of focus.”

Ola has been subjected to criticism for its toxic work environment, which has resulted in numerous employees who are overburdened and underpaid being unable to remain for more than a year. A work environment that is challenging is indicated by personal accounts from employees. Ola recently opted to withhold 20% of the variable compensation that was due to senior management.

In January of the previous year, the organization terminated 200 employees from various departments. When questioned about the rationale for the redundancies, an Ola Cabs spokesperson stated, “We undertake restructuring exercises on an ongoing basis to enhance efficiency, and there are positions that are now redundant.” We will persist in recruiting senior talent in our primary priority sectors, as well as in engineering and design.

Operations may be disrupted, innovation may be impeded, and recruitment expenses may rise as a result of high employee turnover.

Nevertheless, it is important to note that the EV market is heavily reliant on research and development, and the company’s capacity to innovate and remain competitive could be impacted by the loss of skilled talent.

8. No Accountability

The Securities and Exchange Board of India (SEBI) has a history of permitting loss-making businesses to initiate Initial Public Offerings (IPOs), which has led to substantial financial losses for retail investors.

This pattern of regulatory negligence raises significant concerns regarding SEBI’s dedication to its mandate of safeguarding investor interests and maintaining market integrity.

SEBI has a history of allowing loss-making companies to launch IPOs, despite the fact that these IPOs ultimately failed and caused substantial financial damage. This consistent pattern implies that the regulatory body is either grossly incompetent or has the potential to commit malfeasance.

9. No Clear Declaration On How The IPO Proceeds Would Be Utilized

Ola’s huge debt is an obvious warning sign. In the immediate future, the firm says that operational losses will remain, as it concentrates on the expansion of its business and the expansion of its product portfolio. This amount of debt raises valid concerns about the company’s financial stability and its ability to manage long-term liabilities.

Furthermore, the salary structure, which encompasses the founder Bhavish Agrawal’s substantial compensation and sitting fees, may be perceived as excessive and could potentially affect shareholder value.

Aggarwal will be compensated with a base salary of Rs 6 crore per year and a variable pay of Rs 3 crore per year. The yearly compensation for non-executive and independent directors will be Rs 0.5 crores, in addition to Rs 1 lakh in sitting fees.

Ola Electric recognizes the possibility of temporary operational losses; however, it is dedicated to substantial investments in diversification and expansion. The potential for additional financial strain is significant, given that an anticipated ₹1,600 crore is allocated for Research and Development (R&D) over the next three years.

Additionally, research and development should be conducted prior to the release of a product, not later.

The absence of guaranteed returns raises issues regarding the efficacy of Ola Electric’s strategic allocation of funds and the potential for wasteful expenditures.

Hence, despite the hype and the buzz, it is crucial to stay alert and beware of Ola Electric IPO.