Bajaj Housing Finance IPO Analysis: Stocks Soaring—Strong Financials? Sure. But Let’s Give Credit to the IPO Jenga As Well!

Bajaj Housing Finance Ltd (BHFL) had a strong start on the stock exchanges at the start of the week, becoming a multi-bagger on the first day of listing. The stock is listed at INR150, a 114% premium over the issue price of INR70. Bajaj Housing Finance’s IPO broke records by being subscribed 64 times on the last day of bidding and generating bids worth almost ₹3.23 lakh crore, the largest demand in Indian primary market history. The previous record details from October 2010 when Coal India’s ₹15,500 crore public issuance received bids totalling ₹2.36 lakh crore. The IPO also established a new record with 8.9 million applications, beating Tata Technologies’ previous record of 7.36 million.

So, what are the factors that are keeping the investor confidence high in Bajaj Housing Finance Limited? Are these factors really authentic or there is a hidden mist behind all the glitters?

The Goods.

The ancestral worth of the Bajaj group.

Aside from the IPO enthusiasm, factors such as great parentage, a decade of good returns, and future growth potential fuelled the response. The Bajaj Group, which owns some of India’s most valuable enterprises, has consistently generated money for its devoted investors. Its heritage is based on stable returns and good foundations, gaining a reputation for generating long-term value. Hence, Bajaj Housing Finance is seen as another Bajaj brand poised for significant expansion.

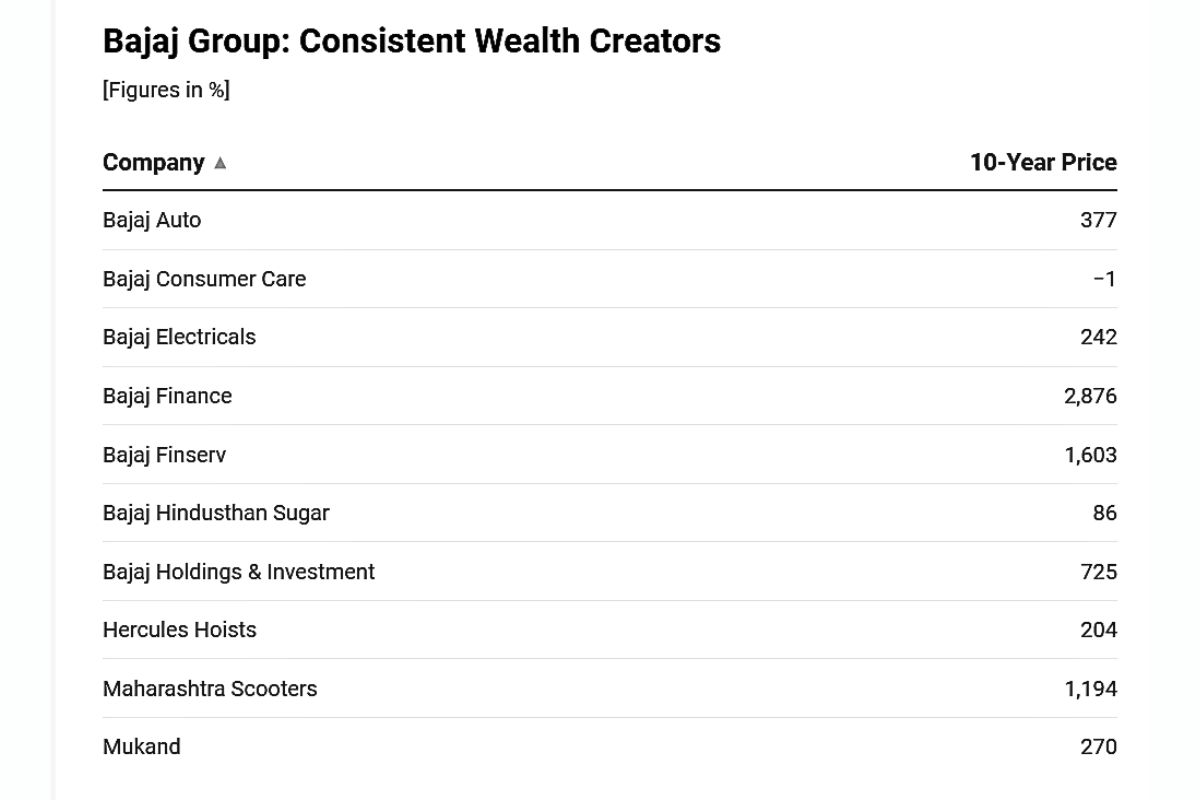

Stocks such as Bajaj Finance, Bajaj Finserv, Maharashtra Scooters, and Bajaj Auto have risen by more than 1000%, transforming early investors into potential millionaires. The group’s flagship firm, Bajaj Finance, has achieved a huge 2876% return over the last decade, making it one of the most renowned companies on the Street. The stock rise has corresponded with robust profit growth for the firm, with profitability increasing at a CAGR of 34% between FY14 and FY24. Sales during the same time increased at a CAGR of around 29.8%.

Bajaj Finserv, the parent company of Bajaj Finance, has likewise rewarded its investors with a 1600% return over the previous decade. While traditional companies like Bajaj Auto and Bajaj Electricals have developed consistently, with 377% and 242%, respectively, the financial arm of the group has been the golden star performer. Bajaj Holdings and Investment’s 725% price rise also demonstrates the group’s capacity to leave a lasting impression across a variety of sectors. Of the 11 group firms on the Street for which data was available, nine produced multi-bagger returns, with two disappointing kids named Bajaj Consumer Care and Bajaj Hindustan Sagar.

According to Incred Equities, Bajaj Housing Finance is projected to continue the success of its parent companies, Bajaj Finance and Bajaj Finserv, which have consistently outperformed the market, with Bajaj Finance being a pioneer in consumer durable financing. So, over the next several years, BHFL expects to expand its AUM by 30% and achieve a ROE (Return on Equity) of 15% or higher. For investors who have witnessed the exponential expansion of Bajaj Finance, Bajaj Finserv, and a number of other firms, as well as those who have missed out, Bajaj Housing Finance represents the next chance to participate in the group’s next phase of growth.

The housing boom of India- a catalyst for Bajaj Housing IPO.

In 2022, HDFC chairman Deepak Parekh made a significant forecast regarding India’s home financing business. He anticipated that India would be able to double its home loans to roughly Rs 46 trillion over the following five years by 2027. Loans to the housing industry increased by over Rs 10 trillion over the two years following the pandemic. However, the RBI estimates that the total amount of outstanding home loans will reach Rs 27 trillion by March 2024. For Mr Parekh’s prediction to come true, home loans will need to nearly double in the next three years. Signalling similar emotions, Bajaj Housing Finance’s recent blockbuster IPO appears to indicate that India’s leading home financers would not look back.

Credit outstanding in the Indian housing finance sector increased at a CAGR of roughly 13.1% from FY19 to FY23. According to BHFL’s IPO documents submitted to stock exchanges, the overall housing finance segment credit outstanding is around INR 33.1 trillion as of fiscal 2024, up 15.2% YoY, driven by the aspirations of a growing young population with rising disposable income migrating to metro cities and elevated demand in tier II and III cities. Hence, the firm appears to be well-positioned to capitalise on the country’s expanding mortgage penetration.

Also, rural development and affordable housing will be significant growth drivers for the home mortgage sector. Credit demand in rural and semi-urban areas for segments such as affordable housing, microfinancing, and tractor purchases could rise as the current government focuses on increasing rural incomes while also improving infrastructure outside of cities.

According to ICICI Securities, a predicted spike in rural credit demand, improved affordability, and the government’s push towards financial inclusion would result in easier rules in the microfinance industry. A credit-linked subsidy program (CLSS) in the Pradhan Mantri Awas Yojana is projected to boost credit development in the future. Bajaj Finance has yet to make inroads into affordable housing, a vast unexplored market for them. And now it’s looking at that segment too.

Better GNPA ratio than peers.

This is arguably the most essential measure for any housing financing company (HFCs). HFCs often have lower NPA ratios than other lenders since the majority of their loans are backed by underlying assets. However, loans against property and developer finance loans might cause complications for lenders. For example, during the COVID-19-induced economic downturn, the GNPAs of the whole housing loan portfolio climbed dramatically from 1.6% in FY19 to 2.3% in FY20 and then to 3.9% in FY21. This resulted in a dramatic decline in HFC stocks during that time. This is a significant risk that investors must be aware of.

However, Bajaj Housing Finance is way better than its peers when compared to GNPA ratios. As on June 30, 2024, BHFL’s GNPA ratio was at 0.28%, as per BHFL’s IPO documents.

- 3.29% for LIC HF

- 1.35% for PNB Housing Finance

- 0.84% for Tata Capital Housing Finance

- 1.36% for Aadhar Housing Finance

- 1.01% for Aavas Financiers

- 1.30% for Aptus Value Housing Finance

- 1.70% for Home First Finance Company India.

Better technology than peers.

The company’s major difference is its use of technology to detect and understand the demands of prospective home loan consumers. Bajaj Housing Finance can reach out to customers faster, allowing them to finish the loan procedure more quickly than rivals. Because financing rates are often the same, technology is the deciding factor. Technology may also aid with risk assessment, debt management, and cost reduction.

One of the most notable examples of using technology to simplify the process dates back to early this year when the firm announced the introduction of its ‘DIY’ application for home loans – an end-to-end digital journey to change the customer experience. The DIY procedure of obtaining home loans allows consumers to have a contact-free journey from application to approval by allowing document upload and bank account verification online.

But every coin has two sides. The hidden behind the mist of IPO frenzy.

The sky-high valuations.

While premium valuations are the norm for well-run firms with trustworthy management, the question of how much arises when an investor’s primary goal is to make profits. At the upper price band of INR70, BHFL stock is worth 3.2x its trailing June 2024 book value. This is more expensive than LIC Housing Finance (1.2x), PNB Housing (1.7x), and Can Fin Homes (2.7x). Analysts, however, are ready to pay a premium for BHFL’s value due to its rapid yearly increase in AUM. This overwhelming demand demonstrates the enormous faith investors have in established business giants such as Bajaj and Tata. These renowned names generate trust, leading to the notion that such investments are almost secure.

However, there are experts who see some criticisms in these sky-high valuations. Sandeep Sabharwal, a prominent fund manager (asksandipsabharwal.com), says the price at which Bajaj Housing Finance is trading is crazy, and there is no way one can justify these valuations. Many organisations in the financial services industry use the same business strategy as Bajaj Housing Finance. It is not a unique sector; it is not like a new technology firm or any of the other businesses listed that one cannot value. This firm is easily valued.

The price at which it is trading is crazy, and there is no way to explain these valuations when huge, established, diversified financials are selling for half, one-third, or maybe 25% of this company’s worth. As with many previous IPOs, this is just frenetic trading in a limited-float company. Sabharwal says there’s a similar frenzy in Ola Electric, which is losing market share every month, it is giving forecasts based on them either maintaining or improving market share, which is not going to happen.

Some analysts feel that the present valuations do not reflect the company’s fundamentals, and that the stock will drop once the froth settles. Even so, they see the stock as a long-term investment. Ambareesh Baliga, an independent market expert, stated that the present market is chasing momentum rather than valuations. If one had been looking at values, they would have seen some corrections. The same thing is happening with Bajaj Housing Finance, where investors are chasing momentum since the fundamentals do not match the present price.

So are the corrections visible; is there any sense of short term profit booking that is challenging the stock?

How many of these IPO applicants can actually be considered investors? A major section of the market consists of traders who are motivated by the promise of rapid profits rather than long-term value.

A SEBI study published at the start of this month revealed that investors sell 54% of IPO shares within a week, reflecting the growing trend of investing in IPOs for listing gains. Investors, in general, display a disposition effect, meaning a higher inclination to leave IPOs with favourable listing gains than those with losses on listing.

The same is witnessed in the last two days, where yesterday’s fall in Bajaj Housing Finance stock price comes after a 4.3% drop witnessed in the previous session. With this, Bajaj Housing Finance shares have fallen more than 11% in two trading sessions, followed by two sessions of healthy gains after listing. This meant that Bajaj Housing Finance shares came under selling pressure at higher levels on Thursday, as investors sought to book profits despite high valuations.

Bajaj Housing Finance shares are anticipated to see short-term profit booking after the rise following the robust listing. While the company’s long-term prospects and the home financing market in India are promising, sustaining the price of Bajaj home financing stock would take time, according to Avinash Gorakshakar, Head of Research at Profitmart Securities. He also adds that the values of Bajaj Housing Finance shares appear expensive based on FY24 results.

Conclusion.

A thriving equities market may provide post-listing momentum for the company, but even blue chips like Bajaj Finance can underperform during macroeconomic downturns. Can equity investors expect their profits to increase as the firm grows? During any euphoria, the immediate returns are obvious; nevertheless, over time, any inflated valuation continues to lower returns despite generating revenues and profit increases.

Similar examples include Infosys and Wipro, which have been running well for decades, but those who invested at the height of the IT bubble in 2000 saw their poorest results in years. Reliance Industries developed year after year, but the returns were low for over a decade following the global financial crisis.

Bajaj Finance, which was trading at a premium and about 7 times the price to book, exemplifies how, despite solid growth, stock returns for years can be depressed when valuations skyrocket. When the benchmark doubled in the last three years, investors saw almost no return. After the IPO celebration, investors may be able to take a closer look at valuations.