Samsung’s Market Share Hits 10-Year Low: 7 Reasons Why The Korean Smartphone Giant Is Losing Ground In India?

Samsung’s dominance in India’s smartphone market is slipping, with its market share falling to its lowest level in a decade as Chinese rivals Xiaomi and Vivo capitalise on the South Korean giant’s frayed ties with offline retailers, reduced presence in the sub-Rs 10,000 handset market, and increased competition in the premium segment. According to data, in the June quarter, Samsung, India’s smartphone market leader until last year, recorded a reduction in volume as well as a major fall in value market share. Traditionally, Samsung had an advantage over its Chinese competitors with its higher-end smartphones, but Xiaomi and Vivo dominated the low-cost smartphone sector.

So what made the smartphone king in India, Samsung, lose its throne to Chinese counterparts?

Market positioning- Samsung is losing ground because of fierce competition from its Chinese counterparts in India’s smartphone segment.

In July, it was reported that China’s Xiaomi reclaimed the top spot in India’s smartphone sector after six quarters, outperforming Korea’s Samsung, which slid to third place behind Vivo in the June quarter, indicating a significant turnaround for Chinese companies in this fiercely competitive market. According to industry leaders, Indian customers can be seen flocking to Chinese electronics brands because they provide value for money and are no longer associated with bad quality, giving them a substantial market share across all sectors. This is despite China’s electronic device businesses being under intensive regulatory scrutiny in India as border tensions rise.

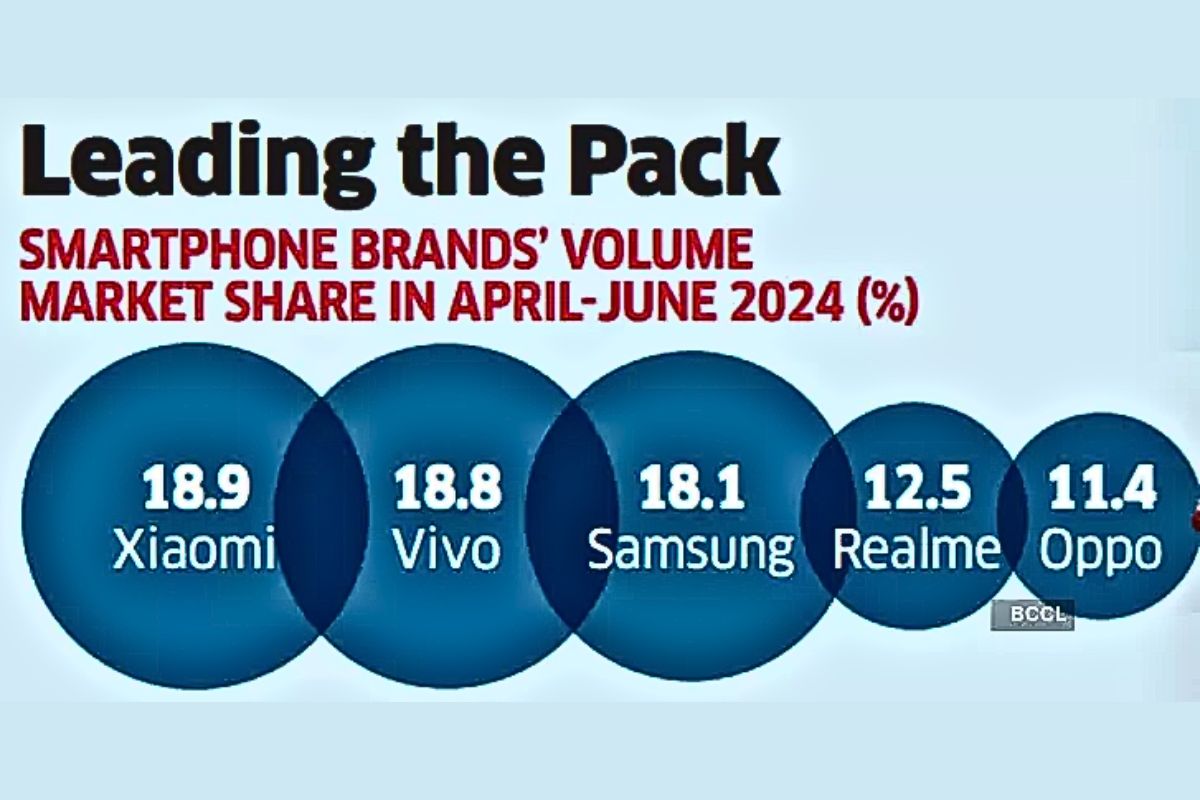

According to Canalys, Xiaomi’s shipments increased by 24% year on year, increasing its market share to 18% in the June quarter from 15% the previous year. Second-place Vivo increased 4% yearly, and its volume share stayed steady at 18%, while third-place Samsung’s shipments declined 8%, with a volume share of 17%. Two more Chinese companies, Realme and Oppo, came in fourth and fifth place, with volume shares of 12% and 11%, respectively.

In the June quarter, the four Chinese top five firms combined for 59% of the market, up from 55% the previous year. According to market trackers, Chinese smartphone firms Xiaomi, Vivo, Oppo, Realme, Transsion, and Motorola increased their cumulative market share to more than 75% in the June quarter, up from a low of 61% in the September quarter of the previous year.

Xiaomi’s fresh surge to the top, as well as the excellent performance of other Chinese firms, demonstrate their appeal in the face of continued Indian government scrutiny. Xiaomi India, for example, is faced investigation by the Enforcement Directorate (ED), which is looking into the company’s payments to third parties since its founding in 2014. The ED has accused Xiaomi of fraudulently sending money to other parties under the premise of paying royalties to its Chinese parent. Xiaomi India denies any wrongdoing.

The company lost its No. 1 title to Samsung in the December quarter of 2022, finally falling to fourth. In fact, in 2022, the company Samsung dominated the market in terms of value, with a 22% share, followed by Apple. Samsung’s rise at the time was ascribed to a focus on growing presence in mainline (offline) retail with higher margins alongside online offers, a desire for premiumisation, the Samsung finance+ scheme, and the great performance of the A series in the Rs 30,000 – Rs 45,000 price range.

Cut to the October–December quarter of 2023. The korean company lost market share to Chinese smartphone makers, and the trend has persisted. According to IDC, Samsung’s market share declined to 12.9% in the April-June quarter, compared to 15.7% the previous year. The company’s unit shipments to distributors and retailers declined 15% year over year. By the June quarter of this year, Xiaomi had regained the top spot owing to its aggressive development in offline retail. Xiaomi, as clever as its country, appears to be capitalising on Samsung’s mistakes and has absorbed most of this lost position. Also, Vivo, another Chinese company, has faced investigations over allegations of tax violations and money laundering.

“Xiaomi appears to have overcome the effects of their prior issues with the ED and top management turnover. Their leadership in India is steadily directing efforts. They have begun to expand their offline channels with a deliberate strategy, beginning in 2023,” says Counterpoint research analyst Shilpi Jain. Additionally, reports have claimed that the company has raised margins for its offline dealers. Customers now have even more confidence due to its internal financing plan,” she continued. She goes on to say, “These days, people choose CMF (colour, material, and finish) when buying smartphones. While Samsung phones lag in CMF, Chinese companies are focussing on the same in their low-cost devices.”

Another person, Nilesh Gupta, director of Vijay Sales, a well-known network of consumer electronics retail chain with locations in Hyderabad, Delhi-NCR, Mumbai, and Ahmedabad, says, “Indians no longer regard these brands as Chinese and consider them international names.” “Over the years, they have established their brand equity in India.”

Inventory Issues harming the Korean smartphone company.

According to Shilpi Jain, Samsung’s M and F series in the below-Rs 30,000 segment underperformed, resulting in a significant inventory buildup. “Samsung’s focus has been on value with premium phones rather than quantity in the mainstream market, where competition is fierce,” Jain explained. Currently, the category below Rs 20,000, on which Samsung is not particularly focused, accounts for around 44% of the whole market, which acted as a catalyst for Chinese smartphone companies.

According to Tarun Pathak, Research Director at market research firm Counterpoint, Samsung’s diminished presence in the sub-Rs 10,000 pricing range has had an even greater impact on its sales. “Samsung has just 6% of its portfolio in the sub-Rs 10,000 bracket, but Xiaomi has three times the market share at 18%. “The yawning gap explains the loss of volume for Samsung,” he added.

The entry-premium market (above Rs 20,000 to Rs 35,000) has a 30% share. According to IDC, the super-premium class of devices costing more than Rs 65,000 has a 6% market share, with Apple leading the way and, hence, again, Samsung getting the rear seat.

On the growth of Chinese brands, Sanyam Chaurasia, senior analyst at Canalys, stated, “Brands such as Xiaomi boosted their mid-to-high-end product lineup, driving volumes for the quarter with the Redmi Note 13 Pro series featuring refreshed colour offerings and the newly launched Xiaomi 14 Civi with its camera quality and distinctive leather design.” Meanwhile, Vivo’s mid-range success was fuelled by the V-series and Y200 Pro, which emphasised improved design and camera features, as well as enhanced push through LFR (large format retail) outlets.”

Brand fatigue causes fatigue in sales of Samsung smartphones.

Faisal Kawoosa, chief analyst at Techarc, stated, “Undoubtedly, there is something known as brand fatigue. Samsung should attempt something different depending on consumer preferences these days. To stay competitive, they should introduce new series or sub-brands such as Xiaomi’s Poco, Vivo’s Iqoo, and so on. Kawoosa used Kia, owned by Hyundai, as an example of how quickly it has acquired market share in India. Hyundai’s Kia launch was a tactic to avoid customer boredom and win the SUV market, and Samsung could consider similar moves to remain relevant.

Dispute with offline retailers.

Aside from brand appeal, Samsung’s concentration on mainline retail channels has recently decreased due to a drop in profits and a tendency towards online channels with pricing disparities and lucrative deals, mobile retailers said. “Retailers continue to voice discontent with margins as well as disparities in pricing and offers,” said Kailash Lakhyani, founder and chairman of the All India Mobile Retailers Association (AIMRA), in a letter to Samsung. “To sustain retailer support, immediate action is required to boost margins and assure price and offer parity,” he continued. This dissatisfaction is undermining Samsung’s key strengths and its relationships with traditional retail partners.

Also, the desire to drift to online sales harms the strong dominance of offline channels. India is one of the few economies where the offline retail channel remains dominant despite the fact that a major portion of the population has embraced e-commerce. It’s also a very competitive smartphone industry, so firms that compete must strike a mix between online and offline selling tactics.

However, retailers in India have begun to believe that Samsung is increasingly prioritising online sales over those from its brick-and-mortar partners. They claim that Samsung is not preserving price parity for specific products, notably the M series, in order to enhance online sales since doing so would not oblige Samsung to provide profits to offline shops. Samsung’s growing emphasis on direct sales via its website, ostensibly at reduced rates, is alienating its larger retail network. While this technique is profitable in the near term, it undermines the underpinnings that have allowed Samsung to dominate the offline market.

Also, in 2020, Offline retailers accused Samsung of misusing user data to shift sales from the offline channel to Samsung.com. Samsung has handed vouchers worth Rs 10,000 each to customers who purchased the Note20 from mom-and-pop shops. “However, such coupons could only be used on Samsung.com,” the AIMRA said in a letter to Ken Kang, Samsung India’s mobile business head. The retailers accused Samsung of sending messages to its pre-booked clients with greater offers and discounts as an “Only for you” offer in which they were promised an extra benefit of Rs 2000, totalling Rs.12,000 if they purchased the pre-booked device from Samsung.com.

AIMRA accused Samsung of using a clear strategy to divert their customers deliberately to the company’s online portals. The company was anticipated to use these data for pitching better deals and offers for all upcoming products to be bought from the company’s portals, which is again unfair, unethical and an absolute breach of trust. Samsung’s differential pricing policy for the online market, where phones are often less expensive, has long been a source of frustration for retailers in person. The attempts to decrease trade margins are discouraging retailers and hurting ties with Samsung’s channel partners.

According to Lakhyani, Samsung is not interested in engaging with retailers or AIMRA. In multiple letters to Samsung’s president and CEO of South-west Asia, JB Park, and Corporate Executive Vice President of the Mobile Division, Soon Choi, AIMRA has demanded that the handset maker increase margins, maintain consistent pricing, offer parity across channels, withdraw selective upgrades, provide sales support, or reduce prices to make business operations easier.

“Mainline sales play an important role in India. Consumers like to buy from companies where they can try out the products firsthand. Samsung’s disobedience for mainline market merchants has reduced their market share to under 14 % [according to IDC], and if they continue with such practices, they will slip below 10 %,” Lakhyani noted. “Samsung is no longer a retail-friendly brand. In comparison, Oppo and Vivo have higher margins.”

Wearable segment- dominated by Indian Brands.

A July end report mentioned that Samsung was worried about its low market share in the price-sensitive wearable business in India and plans to introduce low-cost fitness bands with limited functionality and collaborate with digital organisations and the government to offer wearables as a service. According to an IDC analysis, the wearable device market in India has declined for the first time ever.

The market fell by 10% year on year, reaching 29.5 million units. The smartwatch category continues to suffer, decreasing 27.4% year on year to 9.3 million devices. According to the IDC data, smartwatches’ share of wearables fell to 31.5% from 39.0% in Q2 23. Channel inventory, particularly of previous-generation models, is a major contributor to the reduction. Furthermore, innovation exhaustion is limiting growth for smartwatches.

According to IDC, Samsung owned a 0.5% market share in the total smartwatch segment in India but 15.7% in the advanced smartwatch category in the March quarter of 2024. With a tiny market share, the Korean company placed 11th in smartwatches, trailing mostly Indian competitors offering affordable and lifestyle-centric solutions. Boat continues to top the Indian wearables industry with a 26.7% market share, while Noise and Boult are second and third with 13% and 8.1%, respectively.

Brand Positioning- Samsung sales are anticipated to be affected by Apple’s and Google’s strong movements in India.

Samsung should be concerned about Apple’s rise in India and Google’s growing presence in the country with India-made Pixel devices in the premium tier. In FY24, the value of Apple’s business in India exceeded INR2 lakh crore, which included both export and domestic sales. This was due not just to an increase in iPhone production but also to an increase in domestic sales of the company’s whole product range, which included MacBooks, iPads, and Watches, among other things. The Economic Survey 2023-24 mentions Apple five times, highlighting the company’s prominence in India’s aspirations to become a worldwide smartphone manufacturing powerhouse. Therefore, Samsung must be careful.

The S24 series originally showed promise in the super-premium segment, with AI capabilities putting it ahead of the competition. However, the brand’s share of this category has dropped from 23% to 13% by Q2 2024. With Google Pixel expanding local production in India, Samsung could face more competition, maybe as early as 2024. If AI drives sales, Pixel has the potential to beat Samsung, and even a 1% market share change would result in a huge loss for Samsung.

Last but not least, the loss of key personnel harmed Samsung’s sales.

The company isn’t run on its own; it is being run by a bunch of folks. Kunal Agarwal became the deputy sales head of Xiaomi India in February. He was Samsung India’s senior director in charge of sales, operations, and planning. Following the departure of this seasoned sales leader, some 20-30 regional executives in sales, marketing, and operations left the South Korean company’s India business. Around 10-15 more are anticipated to depart shortly.”

The departure of key individuals to competitors like as Xiaomi appears to be reducing Samsung’s internal capabilities. What began with the loss of a significant individual has now grown, with 1-2 mid-level managers leaving each week. This talent drain may be generating worry among Samsung’s executives, who wake up each day wondering who will be next. It’s not a good feeling when you’re losing share. Xiaomi’s aggressive talent acquisition approach isn’t simply aimed at young people; they just hired the former CEO of Motorola-Lenovo as COO, suggesting a deliberate change towards seasoned leadership.

“This is routine in the industry. According to one source, the departure of 20 of Samsung’s roughly 50,000 employees will not significantly harm the company’s operations. Insiders at the electronics company lowered the number of leavers, estimating that there were about 20 since workers who collaborated with a top executive would frequently follow them to their next position. They went on to say that while nothing is alarming on the inside right now, a slow festive season may make things different.

The bottom line.

It’s critical that Samsung returns to its roots. The brand must prioritise talent retention and address the underlying reasons of talent migration to rivals. The executives that joined Xiaomi appear to have already made an impact. The Chinese company, which is still under official examination for alleged foreign exchange rule violations, has seen remarkable growth in the smartphone sweepstakes since the January-March quarter, owing to increased retail sales.

While internet and direct-to-consumer channels are vital, Samsung’s long-standing strength has been its strong offline presence. The company must find a balance, ensuring that these modern platforms complement, rather than replace, the offline connections that have been critical to its success. Furthermore, Samsung should reassess its product line, notably in terms of design and CMF. Motorola’s revival in 2024, fuelled by a fresh emphasis on CMF, should provide as a valuable case study for Samsung.

Finally, Samsung’s difficulties are diverse and stem from strategy misalignment. Samsung must rapidly rethink its goals and adjust its strategy if it wants to recapture its previous glory and preserve its leadership in this extremely competitive industry.