10 Doubts That Forced SEBI To Hit Out At SME Superstar Varanium Cloud, Imposing A Ban On The Company And Its Promoter From Trading.

A slew of accounting irregularities found by India’s securities regulator recently adds to the risk of a rapid hike in small company shares. Varanium Cloud’s shares nearly lost all their value since its high in October last year. The stock rose to a 52-week high of 239.5 in October 2023 before plummeting to Rs 29.3 in the most recent trading, a drop of up to 87%. The crackdown follows the regulator’s warnings about price manipulation in small IPOs earlier this year. This ban may attract more regulatory action, limiting gains in the S&P BSE SME IPO Index of tiny listings, which has risen more than 5,000% since the beginning of 2021.

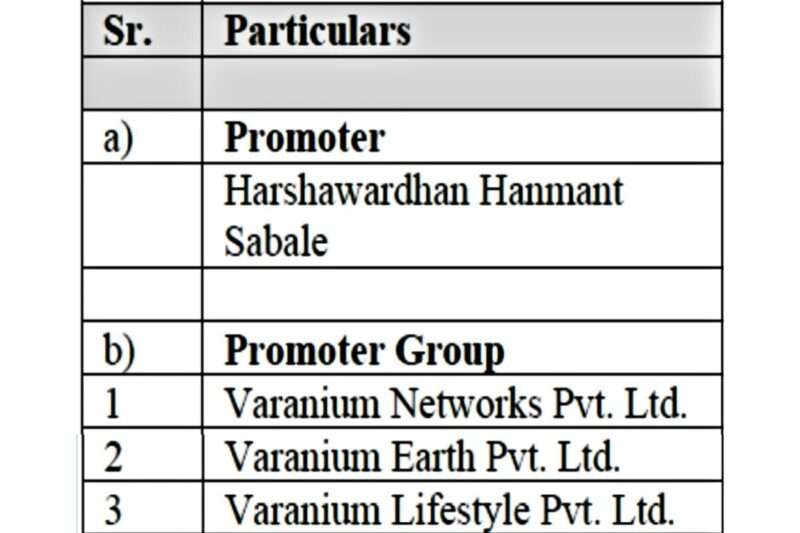

The SEBI, the apex regulatory body, prohibited Varanium Cloud Ltd, an SME listed on the NSE’s SME platform, and its promoter, Harshawardhan Hanmant Sabale, from trading until further orders were issued. Also, SEBI prohibited Mr Sabale from holding senior management roles in publicly traded companies. Varanium Cloud debuted its stock market in September 2022 and quickly became a magnet around investors due to its multi-bagger profits. Four months after the IPO, the shares rose to Rs 1,602 from the offer price of Rs 122.

Part 1—From where it all started—relaxation of rules. Why were SEBI’s stringent rules relaxed for SMEs?

Companies raise funds through IPOs. In return, they sell their shares to the public, ask for cash and list the firm on the stock exchanges. However, not all entities can do this on traditional stock markets like the NSE and BSE. One must ensure that your organisation fulfils the strict standards imposed by the market regulator SEBI. One may need a company whose net worth exceeds a specific threshold. One may need to have a lucrative track record (Although companies that aren’t profitable can still go public under certain restrictions). One may be asked to fulfil more things besides the tasks listed by India’s leading stock exchanges.

That is why going public is challenging, specifically for small businesses or SMEs (Small and Medium Enterprises) looking to develop, grow, and prosper. However, things changed about a decade ago when the NSE and BSE launched separate listing platforms for SMEs. They reduced the laws, making it more easy for small enterprises to enter the market. These businesses did not have to fulfil complicated requirements. And their IPO paperwork did not need SEBI clearance. A positive response from the stock market would suffice. And it worked. Since then, around 950 startups have raised approximately ₹14,700 crore.

However, one needs to know that when the boom comes, the consequences follow. “This is just the top of the iceberg,” asserts analyst Ambareesh Baliga, who has followed Indian stocks for over two decades. Fewer rules were intended to attract high-quality SMEs to the market; unfortunately, they attracted the wrong ones.

These SME’s IPOs have recently gained popularity. In FY24, for example, the number of enterprises using the SME IPO platform reached 205, 64% higher than last year’s figures. They collected roughly three times more money than SMEs that went public in FY23. Listing profits were impressive, often exceeding 300%.

That is why the S&P BSE SME IPO index increased by more than 170% in the past year. This index analyses the performance of over 60 SMEs on the BSE. And it’s no surprise that investors are buying into the hype.

But wait on. There is a catch. However, these high rewards make their entry with high hazards. The most toxic is one SEBI recently identified and is well-known to most SME IPO investors. Here, IPOs are often manipulated. It may comprise personnel from the firm (like promoters) who manage the business and eventually rig the IPO or phoney investors buying these stocks to artificially increase the price, only to dump them on naive retail investors later. Alternatively, a new approach involves creating a firm on paper without an actual business model.

Part 2- How did the company Varanium Cloud misuse the eased rules and regulations?

The Hukum ka Ikka – Marketing!

How did the ‘charm’ of the company worked as a magnet to naive investors?

The company made public statements intended to give naive investors the idea that Varanium was a top-tier IT service provider entering greenfield markets. To provide such an image, Varanium and its promoter engaged in transactions that only emerged on paper. Nothing was happening on the ground, and there was no business-related activity. As presented by the company, no employment was generated.

SEBI states, In the entire sequence of events and the narrative produced by the promoter through public announcements, a favourable feeling was formed, causing many retail investors to purchase the shares. This provided an escape for the promoter entities to make an exit from the company and dramatically cut their ownership at the cost of naive investors. The massive benefits realised by the promoter display the aim and purpose of such public disclosures. These acts benefited only the promoter.

Varanium Cloud made regular announcements with sugar-coated revenue predictions. Because investors cannot see what is happening behind the scenes, it is easy to fall into the trap. These announcements were so effective that the number of shareholders increased from roughly 1,000 to over 10,000 between September 2022 and December 2023, causing the stock price to rise in tandem. Harshawardhan Sabale sold his shares for a whooping ₹122 crores! That doesn’t even include the money he raked in by means of network companies with a promoter part in the firm. That is why SEBI prohibited both the company and Sabale from the stock market.

Investigation by SEBI- 10 Doubts from the lens of the nation’s apex regulator.

Examination Period- September 27, 2022 to March 31, 2024.

Question 1- How did Varanium Cloud spend the money from the IPO?

One would expect the company to use the funds to grow its operations. Obviously, Varanium Cloud confirmed this in its prospectus. As per the prospectus, it established a few data centres, created more digital learning centres, and purchased assets to grow its activities. However, this was an illusion!

In a recent ruling, Ashwani Bhatia, a whole-time member (WTM) of SEBI, stated that it seems that the money received through the IPO and subsequent issuance was not used for the purpose stated in the pre-IPO documents. Instead, the promoter transferred some of the IPOs received to BM traders, whose clarity emerges as doubtful. The SEBI and NSE investigations have made it abundantly evident that Varanium, through its promoter, Mr Sabale, engaged in a plethora of blatantly fraudulent operations to present an image that was inconsistent with the company’s core fundamentals.

Question 2- SEBI investigated how much cash the company had produced after its IPO in FY23.

According to SEBI, all of Varanium’s financial statements include dubious transactions.

- The balance sheet does not decently reflect the company’s financial situation.

- Most sales and buy transactions were simple ledger or book entries. Varanium’s bank a/c statements showed insufficient credit and debit entries to match the alleged sales or transactions.

- The company could not produce supporting documentation for the sales and buy transactions.

Doubt 1- The dubious connection of Varanium and Avance.

According to the SEBI probe, in addition to generating Rs 36.60 crore through the IPO, the company had a pre-IPO placement of 7,00,000 shares to a myriad of shareholders at Rs 99 per share, totalling Rs 6.93 crore. According to the company’s prospectus, it received a quotation from M/s Avance Technologies Limited to build three Containerised Edge Data Centres for Rs 23.40 crore and three Edmission flagship Digital Learning Centres for Rs 8.40 crore, totalling Rs 31.80 crore.

Regarding the same, NSE sought details of quotations received by the company, utilisation of IPO funds (in the form of Statement of Deviation), invoices along with supporting documents like delivery Challan, Goods Receipt Note, agreement with M/s Avance Technologies Limited, and to justify if the company had relations with M/s Avance Technologies Limited. An analysis of Avance’s financial filings displayed that the company is a BSE-listed provider of IT services.

SEBI stated that the value of the quotation acquired by Varanium from Avance (i.e., Rs 31.80 crore) alone exceeded 100% of Avance’s revenue of Rs 30.53 crore reported in FY22-23. Avance’s a/c for Financial Year 22-23 displayed that it had no fixed assets (FA) out of its total assets (TA) of Rs 434.70 crore, with about 96% infused in trade advances, private enterprises, and Jump Networks Ltd.

Avance funded Rs 20.27 lakh in Jump Networks. SEBI found that Jump, now called Winpro Industries Ltd, was a listed firm, with Harshawardhan Sabale as MD from 13 February 2020 to 12 March 2021. According to media sources, Jump (now Winpro) has inked an annual digital services agreement with ‘Amtelfone Incorporated‘ for a minimum guaranteed revenue of Rs 100 crore to deliver wholesale voice-over-internet protocol (VoIP) services.

Due to its lack of FA, Avance’s ability to build the intended Varanium data centres seemed uncertain. Accordingly, Varanium’s accounting of expenditures and payment of Rs 16.98 crore in FY22-23 for developing data centres to Avance out of IPO proceeds is suspicious, SEBI states.

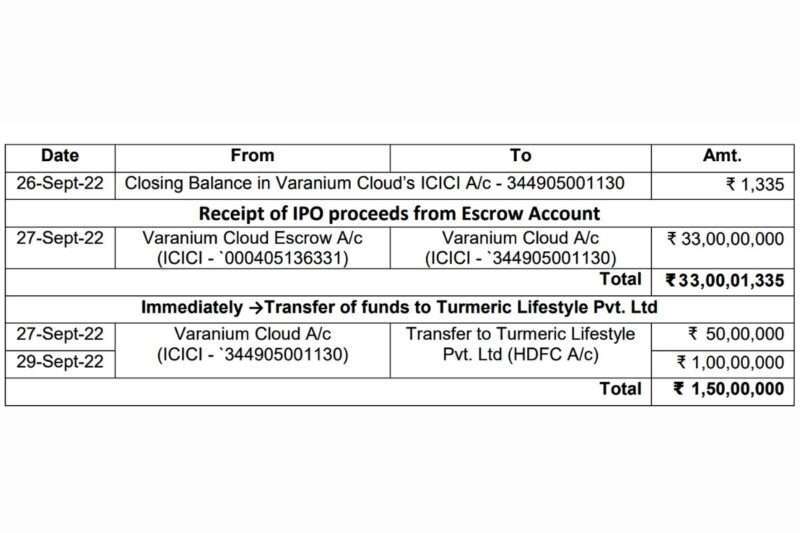

Doubt 2- The doubtful transfer of IPO funds to Turmeric Lifestyle Pvt Ltd (TLPL).

According to Varanium’s financial filings for FY23, Rs.1.83 crore was infused in 3,03,060 Compulsory Convertible Debentures (CCDs) of TLPL out of a total investment of Rs 2.08 crore. Conversely, TLPL mentioned in its MGT-7 filing with MCA that it had granted Varanium 3,03,060 ‘Preferential Shares‘. In addition, TLPL reported no revenue from FY18 to FY23 in its MCA filings. There was no disclosure in Varanium’s Prospectus about the use of IPO funds for investing in TLPL’s CCDs. However, Varanium Cloud Ltd’s bank statement (with ICICI Bank) stated that Varanium sent Rs 1.50 crore to TLPL immediately after receiving net IPO proceeds in its bank a/c.

Regarding the above, Varanium stated in its answer to NSE dated 08-Nov-23 that Varanium Cloud Limited’s investment in Turmeric Lifestyle Pvt Ltd. was an advance. They don’t consider TLPL a linked party since they have no direct influence over its activities or management. According to a contractual agreement with the founder of Turmeric Lifestyle Pvt. Ltd, she is entirely responsible for all operations and management. This highlighted that Varanium’s declaration in its Annual Report for FY23 about its investment in TLPL (classified as Financial Assets) contradicted the NSE filing, in which the payment to TLPL was classified as Advance.

Furthermore, TLPL’s social media handle indicates that the company is in the hospitality sector, renting villas for holidays/staycations in Aldona, North Goa. Its property is listed on Airbnb. As a result, Varanium (a technology firm) and TLPL appear to be in a different line of business, which paves the way for the hazy image of Varanium’s commitment to attaining the objectives of its IPO. It is worth noting that Harshawardhan Hanmat Sabale, MD of Varanium, was a director of TLPL and owned an 83.77% share in the company as of March 31, 2023, according to MCA. According to Varanium’s IPO prospectus, TLPL is a promoter group firm.

Doubt 3- Concerns revolve around gigantic remittances to different entities.

- A review of bank a/c from promoter group firms from ICICI Bank displayed that immediately after receiving net proceeds from the IPO, Varanium transferred Rs 35.81 crore to BM Traders and Rs 14.63 crore to promoter group companies between August 2022 and April 2024.

- Varanium Lifestyle Pvt Ltd also transferred Rs 12.73 crore to BM Traders over the same time.

- Furthermore, Varanium Networks Pvt Ltd sent Rs 67 lakh to BM Traders in March 2024.

- Moreover, a review of Mr Harshawardhan Sabale’s bank a/c statement mentioned that he transferred Rs.119 crore to BM Traders on a net basis.

According to Varanium‘s financial records and annual report, it had no substantial business relationships (either as a customer or vendor) with any of the recipient business indicated above. Accordingly, it was obvious that approximately 60% of the IPO funds were remitted to a company that did not appear to fulfil any of the goals of the company’s IPO.

According to Punjab National Bank (PNB), BM Traders is Raj Kishanchand Jagtani’s proprietary business. The UDYAM Registration certificate of BM Traders, issued by PNB, says that the company was involved in wholesale fruits and vegetables. BM Traders’ declared revenue for AY23-24 was a mere Rs 6,47,200. In a letter to PNB dated April 29, 2024, BM Traders indicated that the company dealt with agricultural products and had no employees. During a site visit to BM Traders‘ business address, PNB personnel discovered it was a residential address with no business activity.

According to SEBI, most of the IPO funds were transferred to BM Traders, which engaged in dubious and suspicious financial transactions with Varanium’s promoter and promoter group entities.

Doubt 4 – A significant jump in revenue from operations raised eyebrows.

The company’s standalone revenue from operations for FY23 was Rs.383.36 crore, a substantial rise of 984.46% from Rs.35.35 crore in FY22. Furthermore, the company’s half-yearly financial results for FY24, i.e., 30.09.23, indicated a revenue of Rs.377.33 crore, nearly similar to FY23.

When asked an answer, the company reacted by noting that “The company has shifted from a B2C (Business to Consumer) model in FY22 to a B2B (Business to Business) strategy beginning in FY23. As a result, revenues from FY23 onwards are gross revenues billed by distributors selling the services in bulk in the MENA (Middle East and North Africa). These contracts are often bulky and enormous in character, resulting in a rise in Gross Revenue. Each similar kind of deal gives substantial revenue, resulting in massive growth. Under this approach, the gross margin (revenues minus data centre costs) would be equivalent to FY22 revenue data, resulting in significantly lower growth.

However, under accounting GAAP, they are compelled to account for gross revenues and data centre costs as stated in the financials, resulting in a considerable revenue hike compared to prior quarters. Also included are all of the GST returns for the regulator’s review. The company also gave a party-by-party breakdown of sales, purchases, trade receivables, and trade payables for FY23 and the first half of FY24.

However, when the NSE sought documents, the firm stated that all paperwork and data files were with the CGST department since the company was undergoing a CGST audit. They would give the complete paperwork whenever they get it from the GST personnel. Mark this statement: The company had given this same ‘GST bahana’ whenever the documentation was demanded by SEBI.

PROBLEMS WITH SALES PARTNERS.

Doubt 5- Here opens another hidden chapter, the company ‘Amtelfone Incorporated’.

In addition, ‘Amtelfone Incorporated’ was a prominent sales partner of Varanium in FY22-23 and the first half of FY23-24. According to public data, Amtelfone’s address is Suite 9, Ansuya Estate, Revolution Avenue, Victoria, Mahe, Republic of Seychelles. If you don’t know, Seychelles is called a tax haven. Many of the firms found in the Panama Papers shared this address. SEBI’s interim ruling states, “Other than those above, no information about Amtelfone has been discovered in the public domain.” According to OpenCorporates, NSE found no firm named ‘Amtelfone Incorporated’.

Varanium’s sales in FY23 totalled Rs 326.22 crores, with 83.91 % going to Amtelfone. In the first half of FY24, the same firm received 71.44 % of Varanium’s sales of Rs 268.1 crore. Varanium Cloud received significant sales from Amtelfone, a firm registered at the location as a company identified in Panama Papers, which is available in the Offshore Leaks Database. During the analysis, it was discovered that a significant number of the firm’s sales in FY23 and the first half of FY24 were made by a company, Amtelfone, which had no online presence other than its peculiar address.

According to Varanium’s response to the National Stock Exchange (NSE), the services given to Amtelfone, a distributor of VoIP services in the MENA, were VoIP services on a wholesale SoftwareAs-A-Service (SaaS) basis. Because there was limited information about Amtelfone, the NSE sought invoices and signed agreements with the client firm. In response, Varanium gave the same ‘GST bahana’ that all paperwork and data files were with the CGST department owing to an ongoing CGST audit. They would give the complete paperwork whenever they get it from the GST personnel.

The ledger records for transactions with Amtelfone show that sales entries were entered monthly, but no bank receipt entries were updated in FY23. Instead, there were only changes to journal entries for Secur Credentials Ltd and Amazon Web Services. The law enforcement officers also discovered a disparity in trade receivables records.

According to the company’s split of Trade Receivables, Amtelfone’s outstanding balance on 31-Mar-23 was Rs 60.21 crore. However, according to the ledger, the amount stood at Rs 85.94 crores as of March 31, 23. As a result, the Trade Receivables reported by the Company in Amtelfone’s ledger do not match the data the company gave. It is worth noting that the company has recorded payments from Amtelfone in its ledger. However, Varanium’s Bank Statement of ICICI A/c No. 3449050001130 revealed no comparable credit entries in the name of Amtelfone, as indicated in its ledger. This sparked suspicions.

Given the anomalies between Amtelfone’s ledger and the company’s filings, it seems that the company’s sales transactions with Amtelfone and the noteworthy hike in revenue claimed by the company were erroneous.

Doubt 6- One more mismatch with another sales partner, Cressanda.

Varanium had made sales of Rs 21.07 (5.42% crores in FY23) with Cressanda. According to Cressanda’s annual report for FY23, “Cressanda Solutions Limited, an India-based firm, is found involved in the domain of information technology, digital media, and IT-enabled services.” Cressanda’s revenue increased dramatically, from Rs 0.18 crore in FY22 to Rs 75.13 crore in FY23. Furthermore, according to Cressanda’s Annual Report for FY23, the revenue of Rs 75.13 crore came from ‘Trading Sales’, with Rs 71.77 crore reported as ‘Purchase of Stock-in-Trade’. However, according to Varanium’s Annual Report, all sales were for the services given.

As a result, there appears to be a discrepancy in the a/c of Cressanda and Varanium, where Cressanda has documented the purchase of “stock-in-trade”. At the same time, Varanium has recorded the sale of “services” for the same transaction, raising doubts!

Doubt 7- Money transferred to the To-be striking-off company raised doubt.

Varanium made sales of Rs 0.30 crores (0.07% total) with Shree Refrigerations Pvt. Ltd. in FY23. According to MCA, the firm above is based in Maharashtra and is now in the process of “striking off.”

Doubt 8 – Sales with a company that does not match Varanium’s line of business.

Varanium made sales of Rs 107.16 crore (28.56 % of the total) with CCL (Courage Clothing LLP) in the first half of FY24. According to the CCL ledger given by the Company, Varanium reported a single accounting entry for sales of Rs 107.16 crore, with the total amount unpaid as of December 31, 2023. Varanium’s line of business did not match the stated export of products claimed on CCL’s a/c. Furthermore, the company did not provide sales-related records.

A public search yielded no results for Courage Clothing LLP. Following this observation, the NSE asked for all invoices and agreements with CCL from Varanium, to which Varanium gave the same ‘GST bahana’. So, Varanium’s claimed sales to CCL seemed phoney.

Doubt 9 – Leave the act of transactions with other companies; three ‘companies working under the same management’ also raised doubts. Huh!

Varanium reported sales of Rs 23.36 crore (6.01% of the total) in FY 2022-23 with VLPL (Varanium Lifestyle Private Limited). Varanium’s annual report lists VLPL as a related party under the category “Companies under the same management.” VLPL is also a Varanium promoter group business established on April 22, 21. Employee benefit expenses at VLPL grew significantly from Rs 1.45 crore in FY22 to Rs 18.38 crore in FY23. VLPL’s RPT reports show that remuneration for KMPs grew from Rs 1.26 crore in FY22 to Rs 17.61 crore in FY23. Harshawardhan Sabale, MD of Varanium, owns 83.01% of VLPL and is a crucial management partner.

According to the VLPL ledger for FY23, the initial credit balance was Rs 2.33 crore. Only two sales transactions were registered in FY23 (December 31, 2022, and March 31, 2023), totalling Rs 23.35 crore. Varanium made purchases of Rs 2.6 crore in the same a/c within the same period. After revising all of the prior entries, the outstanding debit amount in the ledger of VLPL as of March 31, 2023, was Rs 20.85 crore, which got slashed to Rs 12.63 crore as of 31.12.23. The company’s reported sales of Rs 23.36 crores to VLPL in FY23 first seemed doubtful and suspicious.

Varanium reported sales of Rs 11.80 crore (3.03% of the total) with VNPL (Varanium Networks Private Limited) in FY23. VNPL’s revenue in FY23 was Rs 0.41 crore, with no purchases and additional expenses amounting to Rs 0.21 crore. However, Varanium reported sales of Rs.11.80 crore to VNPL simultaneously, which differed from the value shown in VNPL’s a/c.

VNPL’s CWIP rose by Rs 10 crore during the same fiscal year. The rise was not due to transactions with Varanium since none were revealed in VNPL’s RPT declaration. It was also found that in FY23, VNPL got a loan of Rs 11.52 crores from entities under the same management, including Varanium. Given the concerns above, Varanium’s stated sales of Rs 11.80 crore to VNPL in FY23 look suspect.

Varanium reported sales of Rs 5.90 crores (1.52% of the total) to VEPL (Varanium Earth Private Limited) in FY23. VEPL’s employee benefits expenses grew from Rs 5.91 crore in FY22 to Rs 6.97 crore in FY23. The remuneration of the Director at VEPL went from Rs 5.64 crore to Rs 6.60 crore, while the Employee cost-to-sales ratio climbed from 24.75% to 76.40% in FY23 compared to the last fiscal. Based on the aforementioned findings, Varanium’s sales of Rs.5.90 crore to VEPL in FY23 seemed doubtful and suspicious.

PROBLEMS WITH PURCHASES.

Doubt 10 – Compromising nature of purchases.

Varanium made purchases of Rs 201.85 crore (77.79% of total) in FY23 and Rs 243.53 crore (100%) in the first half of FY24 from AWS (Amazon Web Services India Pvt. Ltd). According to the company’s answer to the NSE, AWS provided Varanium with “bare metal server hosting and data managed solutions.” To authenticate the transactions, the NSE sought all agreements/contracts and invoices from Amazon Web Services, to which the company answered with their favourite ‘GST bahana’.

The AWS ledger showed no payment records. However, the adjustment journal entries were created for one of the sales parties, Amtelfone Incorporated, showing that sales and purchases had been offset. AWS’ ledger from April 1, 2023, to 31.12.23 also revealed no payment entries for nine months of FY24. According to the Trade Payables breakdown, the sum due for AWS as of September 30, 2023, was Rs 20.82 crore.

However, according to the ledger, the outstanding sum as of September 30, 2023, was Rs 243.50 crore. As a result, there is a discrepancy between the Trades Payable amount shown in the financials and the shared ledger copy, casting questions on the legitimacy of transactions made using AWS, totalling Rs 243.50 crore. As the Company failed to submit supporting papers for the purchases made from AWS, the legitimacy of the stated purchase transactions in FY23 and the first part of FY24 could not be established.

Furthermore, Varanium made transactions of Rs 33.88 crore (13.06% of the total) with SCL (SecURCredentials Ltd) in FY23. According to SCL’s financials for FY23, its revenue from operations was Rs 50.01 crore. Varanium generated nearly 68% of SCL’s revenue in FY23, receiving services from SCL worth Rs 33.88 crore.

Varanium only paid Rs 0.25 crore to SCL, and the remaining was deducted from the sale of IT services and rectified through a journal entry with ‘Amtelfone Incorporated’ (a sales party). This calls into question the veracity of Varanium’s said acquisitions of Rs 33.88 crore in FY23. Furthermore, Varanium and SCL are not in the same line of business, and Varanium did not have so many workers to justify such big payments to SCL for background verification services.

The bottom line.

It’s important to note that the company often responded that it was conducting CGST audits when questioned about supporting documentation for its claims. Their documents are in the CGST department, which houses all data files and documentation. When the firm receives the whole set of papers from the GST staff, they will provide them. This statement, ‘GST bahana’, is non-satisfactory. The above ten doubts discussed are not only the suspicious acts by this company; the list has many more things. We have discussed the reasons which have probably been at the centre for raising concerns by SEBI.

In lieu of a myriad of inconsistencies found across multiple a/c in the Company’s financial books and other findings (discussed above), the authenticity of Varanium’s financials, including Sales and Purchases, mentioned in the Company’s books of a/c, emerges as dubious. According to SEBI, the prima facie observations and results clearly show that Varanium misused the IPO funds and falsified its financial statements by declaring bogus sales and transactions. The misstated financial statements painted a rosy image of the company’s financial health. In the next months, SEBI will publicise what punishment it will inflict on this corporation if found guilty and what rules it will implement to ensure that others become vigilant about their actions.

However, it is keeping a close eye on these SME IPOs. SEBI realised that companies openly exploit this listing approach to extract massive profits while leaving unwary investors in the bag. And it may soon impose stronger laws to combat their misbehaviour. Could this backfire on SMEs looking to grow genuinely? We hope not, but time will tell.