Ola IPO: Product Faults And No Profit Pathway; Investors Should Proceed With Caution while Investing

EV manufacturer Ola Electric has received approval from the market regulator SEBI for its initial public offering (Ola IPO), aiming to raise Rs 7,250 crore.

In December, Ola Electric submitted a draft red herring prospectus (DRHP) to SEBI, proposing to raise up to ₹5,500 crore through a fresh equity issue, with a target valuation of USD 5 billion. Additionally, the company plans an offer for sale (OFS) of 95.19 million equity shares, each with a face value of ₹10. Founder and CEO Bhavish Aggarwal intends to sell the largest portion, offering 47.3 million shares, which is half of the total shares for sale.

According to the DRHP, the funds from the Ola IPO will be allocated for capital expenditure, debt repayment, and research and development (R&D). Specifically, approximately Rs 1,226 crore will be used for capex, Rs 800 crore for debt repayment, Rs 1,600 crore for R&D, and Rs 350 crore for inorganic growth.

Notable Problems With Ola IPO

In the fiscal year 2023, Ola Electric reported a net loss of Rs 1,472 crore, with operating revenue of Rs 2,631 crore. For the first quarter of FY24, the company recorded a net loss of Rs 267 crore on operating revenue of Rs 1,243 crore.

ANI Technologies, which operates the ride-hailing segment, reported a loss of Rs 1,082 crore in FY23, a significant reduction compared to the previous year. The revenue for ANI Technologies increased by 58% to Rs 2,135 crore in FY23. Does it make sense for a loss-making company like Ola to release an IPO?

A notable aspect of the Ola IPO is the large number of shares being sold by promoter Bhavish Aggarwal in the OFS. He plans to offload 4.73 crore equity shares through the IPO. Given that Aggarwal, the primary promoter with the largest shareholding, is selling nearly 50% of the shares in the OFS, questions arise regarding his confidence in the future prospects of Ola Electric.

Before the Ola IPO listing, Aggarwal held a 36.94% stake in Ola Electric, while ANI Technologies and Indus Trust owned 4.35% and 3.85%, respectively.

Significant shareholders reducing their stakes in Ola Electric post-IPO include SVF II Ostrich (21.98%), Alpha Wave Ventures II (3.49%), Internet Fund III (6.03%), and MacRitchie Investments (1.25%).

The primary issue with the DRHP is that despite the company’s current losses, there is no clear path or strategy outlined for achieving profitability. Investors typically seek at least a roadmap to profitability, if not immediate profits, when considering an investment in a company.

Fundamental Problem With The Business Model

When you compare the GDP per capita, the US stands at USD 70,000 and China at USD 12,000, while India’s is around USD 2,200 (approximately INR 1.8 lakh per year). Ask yourself – how many cab rides could someone earning 1.8 lakh annually afford? Maybe once a month, on a good day?

However, thanks to the substantial discounts offered by Uber and Ola, even a person in this income group was able to take a cab every week, as it was either free or cheaper than an auto-rickshaw.

This phenomenon was labelled as “market disruption”, on which these companies thrived. The truth is that the “disruption” was nothing but burning cash in crores. Figures suggest that Uber and Ola have collectively burned over INR 30,000 crores.

As the funding environment got stringent, cash-burning became more difficult , and investors started demanding profits. So, discounts reduced, and thus, people switched back to public transports and rickshaws from cabs.

To summarize, the service is not struggling because the companies have become complacent; it is because the business model was never intended to scale this much. It works beautifully as a niche service for the wealthy class who can afford the true cost of an air-conditioned cab without hesitation (or maybe with some hesitation).

This service was never genuinely “for everyone,”. It just seemed so because the money from venture capitalists was flowing in, allowing these companies to burn cash in abundance in the name of “making business” and “acquiring users”.

Startup enthusiasts often say that these investments are made with the “future” in mind. The firm belief that these “habit-forming” services will eventually become profitable when India’s discretionary spending increases. In essence, the business model relies on a future scenario that may not even occur. The path to profitability is actually a big probability, with the company being at odds.

What income level would make an average person be willing to pay a premium for such luxuries? A per capita income of USD 6,000 (INR 4,80,000 per year). That is at the current levels. In the future, this number would increase keeping inflation in mind.

GDP per capita is essentially a nation’s GDP divided by its population. To achieve a GDP per capita of USD 6,000, India’s GDP would need to reach nearly USD 10 trillion, assuming the population stays constant. According to Prime Minister Modi, India could become a $5 trillion economy by 2024-25 or by 2028-29. Even if that happens, the GDP per capita, a more accurate measure, would still be low for an average person to use these services.

Some argue that the national GDP per capita is too broad a metric and suggest focusing on the GDP per capita of metropolitan cities like Delhi, Mumbai, Pune, Bangalore, Chennai, Hyderabad, and Kolkata.

Looking at Delhi, the GDP per capita is over USD 5,000. But, can a metropolitan city truly be a correct benchmark? How many cities in India are like that? At most four, with a combined population of less than 100 million.

How does this support the investment thesis of “capturing a market of 1.3 billion people”? How does it justify the over USD 4 billion in cumulative losses incurred by Ola and Uber? Moreover, if operating in metro cities was the strategy all along, why is Ola operating in 160 cities?

Wouldn’t Ola Autos be a better fit for India? Operating cars at such a scale never made sense (and still doesn’t). In five years, Uber and Ola could be promoting Autos more than ever. This shift is understandable.

Flawed Product

At its launch, Ola Electric claimed to have sold over 100,000 scooters on the first day, even before the product was ready for delivery. The company promised to deliver the scooters within a month, but they failed to meet this commitment, continually delaying deliveries. They attributed this to the semiconductor chip shortage, but if production wasn’t prepared, why promise a one-month delivery timeline?

Ola reported a driving range of 195 km for its S1 Pro model and 151 km for the S1 Air. However, the actual range is about 40% less (130 km for the S1 Pro and 90-100 km for the S1 Air), and decreases further with a passenger. Ola has been accused of misleading consumers by only showcasing the certified range, which is tested in a lab. Indian road conditions significantly reduce this range.

In contrast, Ola’s competitors like TVS and Ather provide accurate range information, with TVS disclosing a true range of 100 km for its electric scooter.

Ola gained significant market share in the two-wheeler EV segment by offering substantial discounts. However, fundamental issues with their products and the entry of established players like Bajaj and TVS are now posing challenges for the company.

In April, images circulated of a blue Ola S1 Pro with its front wheel detached after a head-on collision in Maharashtra, raising concerns among Ola’s suppliers. The S1 Pro’s front fork arm failed under tough Indian conditions.

In two-wheelers, the suspension unit is crucial for handling rough terrain and ensuring a smooth ride. Ola’s front fork arm, made from high-pressure aluminium die-casting, connects the suspension to the wheel using a cantilevered design, supported only on one side. This design is unique in India’s two-wheeler market.

In some instances, the arm broke when the rider applied the brakes suddenly. As more incidents emerged, it became evident that the scooter was designed for smooth and traffic-free European roads, and is heavily unsafe for true Indian conditions.

The Ola S1 Pro’s design is inspired by Dutch-EV maker Etergo’s Appscooter. Taking inspiration is one thing, but Ola did not make efforts to change the design for Indian conditions.

When the first incident was reported on social media, Ola had fewer than 50,000 scooters on the road. This was a chance to address the problem, but the company chose not to redesign the part, which would have required significant changes. Instead, they continued to increase production.

“This would have been an opportunity to slow down, review processes, address issues, and then gradually resume production — which is what a responsible original equipment manufacturer (OEM) would do,” said a source.

There were also reports of the scooter suddenly switching to reverse mode, causing multiple accidents. Ola did not acknowledge the issue or announce a recall to fix this serious software problem.

Brands can make mechanical or engineering errors, which are mostly rectified through a recall mechanism. This shows that the brand is committed to passenger safety at the stake of its own reputation. In the case of Ola Electric, the brand seems more focused on maintaining its image as a disruptive and innovative scooter maker rather than ensuring passenger safety.

Insufficient Number of Service Centers

A product needs regular and timely maintenance, especially if it has flaws. Ola Electric struggles with insufficient service capacity, having just over 400 service centers across the country. At any given time, there are about 8,000 open service requests and nearly 1,000 scooters waiting for repairs.

How is Ola Performing Worse Than Uber?

The pandemic was a challenging period for all cab companies globally. During this time, Ola chose to focus on the EV segment and left its core operations to run on an autopilot pilot. This was a bold move, considering that the company was making heavy losses.

This decision led to many drivers leaving the company, resulting in fewer cabs on the roads. This gave Uber an edge.

Back in 2017-18, many individuals joined Ola and Uber as drivers due to attractive incentives, with some even leaving stable jobs. However, the pandemic severely impacted these drivers. The income from driving cabs suddenly reduced but the expenditures were still going on (even increased for many as they faced hospital bills). Ola failed to provide a stable income, forcing many drivers to return to their hometowns. Consequently, the number of cabs on the roads decreased significantly.

The pandemic was not the only problem for Ola cabs. The company also reduced driver incentives to improve their profit margins, leaving drivers with meagre earnings, making quitting an easier option for them.

According to sources, Ola’s revenue sharing and calculation methods with drivers are unclear, unlike Uber’s. These issues severely impacted Ola’s top line, with revenue dropping by more than 60% in FY21.

Jack of All Trades, Master of None? More Like Jack of None, Master of None

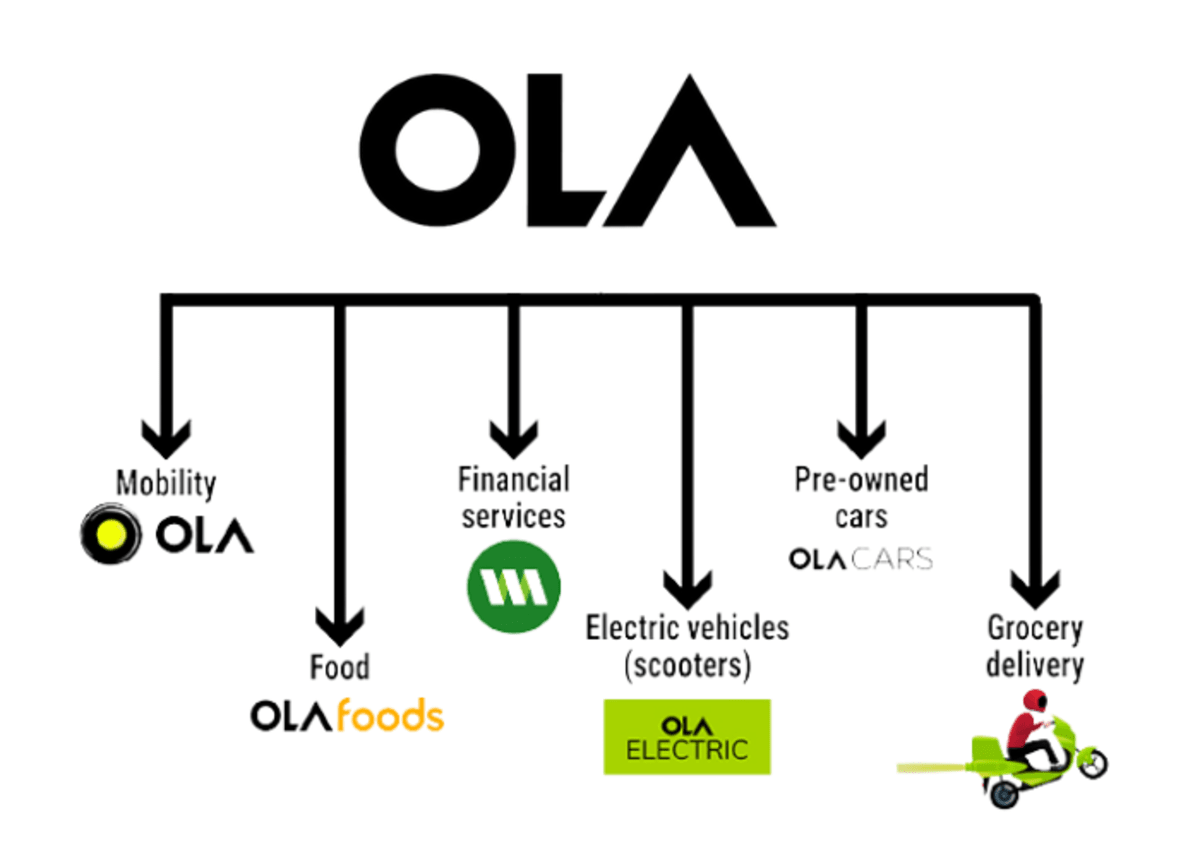

The first major issue with the company lies with its CEO, who has been described as aggressive and overly ambitious, wanting to dominate multiple unrelated ventures. This has led Ola to burn through cash on various failed projects, such as Ola Money, Ola Cars, and Ola Foods. You might not be familiar with these businesses because successful products gain attention, whereas unsuccessful ones often shut down quietly.

In 2015, Ola launched Ola Cafe, which shut down after almost a year. In 2017, it acquired a 95% stake in Foodpanda for INR 200 crore and further invested INR 1,200 crore. Foodpanda then acquired Holachef, but by 2019, both companies were shut down. This was done in an attempt to compete with UberEats by Uber, which also failed in India and was eventually sold off to Zomato in 2020.

In December 2021, amid the hype surrounding the grocery delivery business, Ola launched Ola Dash. However, the company quickly realized the challenges and scaled down the operation, resulting in over 2,000 layoffs.

Ola also ventured into the used car market with Ola Cars, wherein it aggressively promoted the platform for buying and selling used vehicles. However, customers reported multiple issues, such as high prices and low-quality and unreliable cars, leading to plans to shut down operations in many cities.

The company has spent a lot of money on these ventures but has failed to achieve genuine success.

Ola’s Four-Phase Business Strategy Does Not Seem To Be Working Out

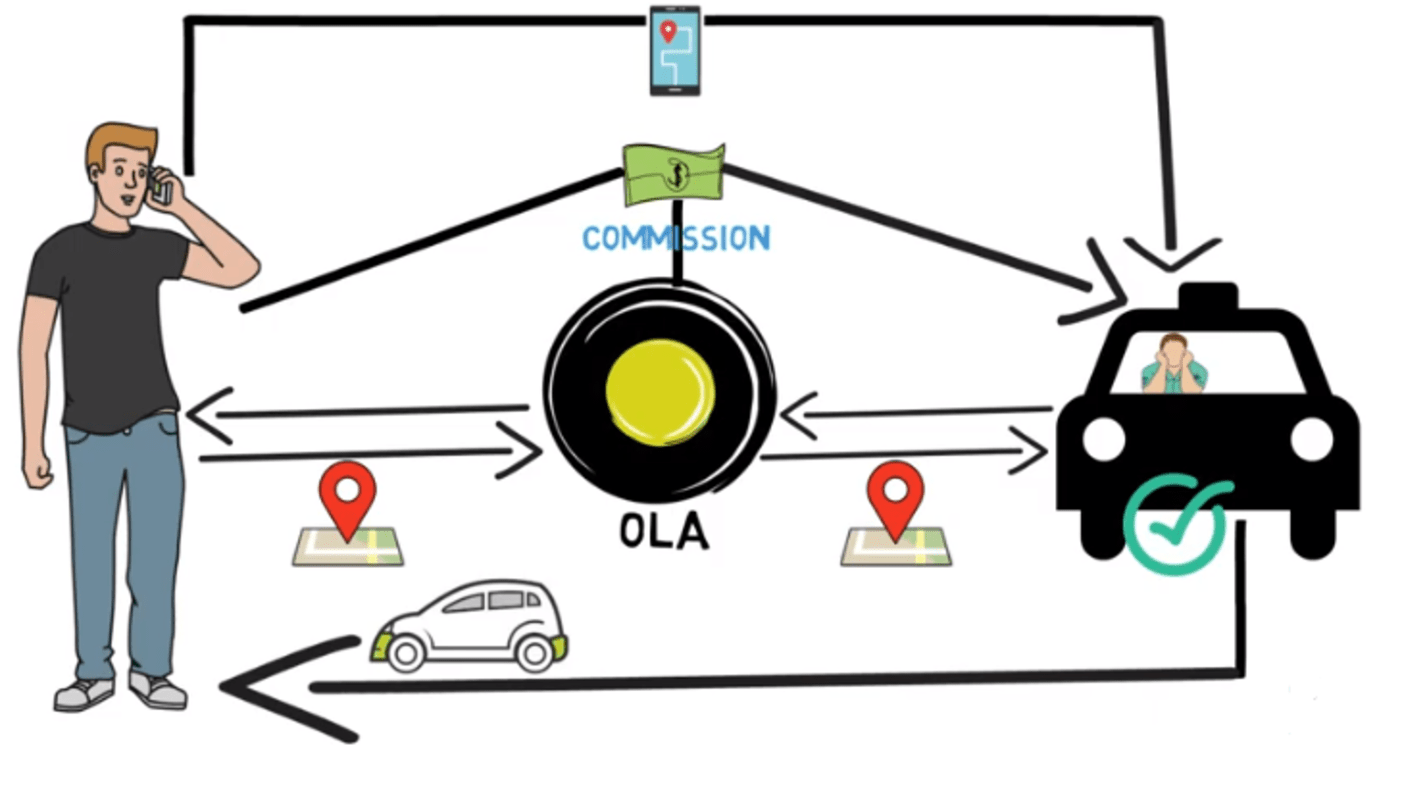

Ola leverages the network effect to fuel their market growth, using a strategic 4-phase framework. Let’s break down each phase:

Phase 1: Cash Drain

To attract both drivers and customers, Ola implemented a cash drain strategy. They offered substantial discounts to customers, making cabs more appealing than auto-rickshaws. Simultaneously, they provided lucrative rewards and incentives to drivers, who could earn around INR 70-80K per month on an average.

Phase 2: Trust Building

Ola built trust among drivers, leading many from lower-income groups to leave their jobs, take loans, buy cars, and start working as Ola drivers. Customers, meanwhile, became accustomed to using Ola for their travel needs.

Phase 3: Dependency

Drivers who left their previous jobs, took loans from the banks or even unofficial lenders, and bought cars found themselves heavily dependent on Ola until they could repay their loans. This snatches away all the leverage from them and reduces their bargaining power.

Customers, encouraged by initial heavy discounts, also became highly dependent on Ola to travel from one place to another. During this period, many traditional cab services either went out of business because they could not offer such heavy discounts to users and eventually losing in price wars. Many also merged with Ola (and also Uber), shifting the Indian cab service landscape towards these two companies, creating an oligopolistic situation.

Phase 4: Control

With both drivers and customers now dependent on their services, Ola and Uber gained significant control. They reduced driver incentives and introduced surge pricing for customers, aiming to boost profitability. However, this strategy backfired, causing pain for both drivers and customers, and ultimately for Ola as well.

Supply Side Challenges

During the Control phase, driver incentives were slashed by nearly 60%, and rising petrol prices further cut driver earnings by over 50%. The pandemic highlighted these issues, bringing cab operations to a long pause and depleting the hard-earned drivers’ savings. It forced many people to return to their villages.

Many cars were seized by banks due to loan defaults, and banks grew wary of issuing loans to new drivers. As a result, drivers turned to car lenders, who own multiple cars and rent them to drivers on a profit-sharing basis (usually, 60:40). This means that for every INR 30K profit, INR 18K goes to the driver and INR 12K to the car lender.

The pandemic also deterred lower-income groups from joining the cab business, as they witnessed the struggles and protests of cab drivers. Consequently, even post-pandemic, the number of people rejoining as cab drivers remained low.

Another factor impacting Ola and Uber was the rise of delivery companies like Dunzo, Swiggy, and Zomato, which attracted many former cab drivers. The cost of owning and maintaining a bike is much lower than that of a car, and the flexibility allows for easier job switching. Thus, many drivers preferred delivery jobs, especially since these companies were in the cash drain phase, offering substantial incentives.

This shift in incentives from Ola and Uber to quick commerce companies led to a significant shortage of cabs and drivers, compounding the problems for both ride-hailing giants.

Stagnating EV Volume In The Indian Market Also Poses A Challenge

The electric two-wheeler market in India has seen stagnant volumes over the past three months. Registrations for high-speed electric two-wheelers dropped by 27% in May compared to the same period last year. This decline follows a rush in pre-purchases driven by the government’s decision to significantly cut FAME-II subsidies for electric two-wheelers starting June 1, 2023, which had previously lowered prices.

Since April, the government has further reduced subsidies as part of a transitional policy intended to bridge the gap between the end of FAME-II (on March 31, 2024) and the upcoming implementation of FAME-III.

In May, Ola Electric dominated with a 48% market share. Despite this, electric vehicles (EVs) only accounted for 5% of the overall two-wheeler market, maintaining similar levels to last year.

Investors are increasingly concerned about future growth drivers for electric two-wheeler startups. An investor involved in an IPO, who wished to remain anonymous, stated, “We are looking for the next growth trigger in the e-two-wheeler market. The stagnation in volumes over recent months has shifted the focus back to profitability and efficient capital use for EV companies.”

“With FAME-III on the horizon, the amount of subsidies for e-two-wheelers is likely to decrease further, making these factors even more crucial in evaluating the sustainability of these businesses,” the investor added.

The electric scooter market is becoming more competitive as established players like TVS Motors and Bajaj Auto increase their market shares to 19% and 12%, respectively, in FY24.

Terrible Work Culture And High Attrition Rate

Ola Electric is preparing to lay off approximately 400-500 employees as founder Bhavish Aggarwal is diverting his efforts towards the control of operating costs as the company is listing its IPO.

The parent company of Ola Cabs, Chief Financial Officer (CFO) Karthik Gupta resigned on May 16, just seven months into his role. This followed the departure of Ola Cabs’ CEO Hemant Bakshi, who left after only four months, suggesting potential internal challenges.

According to the DRHP submitted to SEBI, Ola Electric’s employee attrition rate was 47.48% for the fiscal year ending March 2023. In January of the previous year, the company had laid off 200 employees across various teams.

When asked about the layoffs, an Ola Cabs spokesperson stated, “We regularly conduct restructuring exercises to improve efficiencies, and there are roles which are now redundant. We will continue making new hires in engineering and design, including senior talent in our key priority areas.“

Ola has faced criticism for its toxic work culture, with many overworked and underpaid employees unable to stay for over a year. Personal accounts from employees suggest a challenging work environment. Recently, Ola decided not to pay out the variable compensation to senior management, withholding 20% of their compensation.

Last year in January, the company had fired 200 employees from the company across different teams. When asked about the reason behind the layoffs, Ola Cabs spokesperson told, “We regularly conduct restructuring exercises to improve efficiencies, and there are roles which are now redundant. We will continue making new hires in engineering and design including senior talent in our key priority areas.”

Those in the industry are aware of the toxic work culture of Ola. Many overworked and underpaid employees are not able to hold for over a year. On a personal level, I have four friends working there, one of whom recently opened up about the work culture. While the majority of the conversation took place on voice call, this chat snippet should tell you enough.

Ola Cabs Prepares for IPO

With Ola Electric’s IPO approved, its Cabs division also plans to submit Ola IPO papers to the Securities and Exchange Board of India (SEBI) within the next three months. Backed by Japanese VC firm SoftBank, Ola is currently in discussions with multiple investment banks, including Goldman Sachs, Bank of America, Citi, Kotak, and Axis, with the intent to finalize the selection of IPO advisors within a month.

This marks the second attempt at Ola IPO, following a failed effort in 2021 to raise USD 1 billion. In 2021, Ola was valued at USD 7 billion during a fundraising round, but its investors have since lowered its valuation in internal assessments. Vanguard, a shareholder of Ola, reduced its internal valuation of the company to USD 1.9 billion in February.

Additionally, Ola Cabs has shut down its international operations in Australia, New Zealand, and the UK. The company cited the reason for the same to focus on the India business, as it seems to be fast-growing.

Summarizing it all, lack of pathway to profitability, consistent losses, changes in the macro environment, horrible work culture, shut down of international business, competitors coming in the EV sector, and most importantly, a flawed business model, makes Ola IPO a risky investment.

Invest with caution!