GST Chronicles- The Tale Of Vadas And Popcorns!

One nation one election, BUT, multiple GST for similar items- The Splendid tale of GST chronicles!

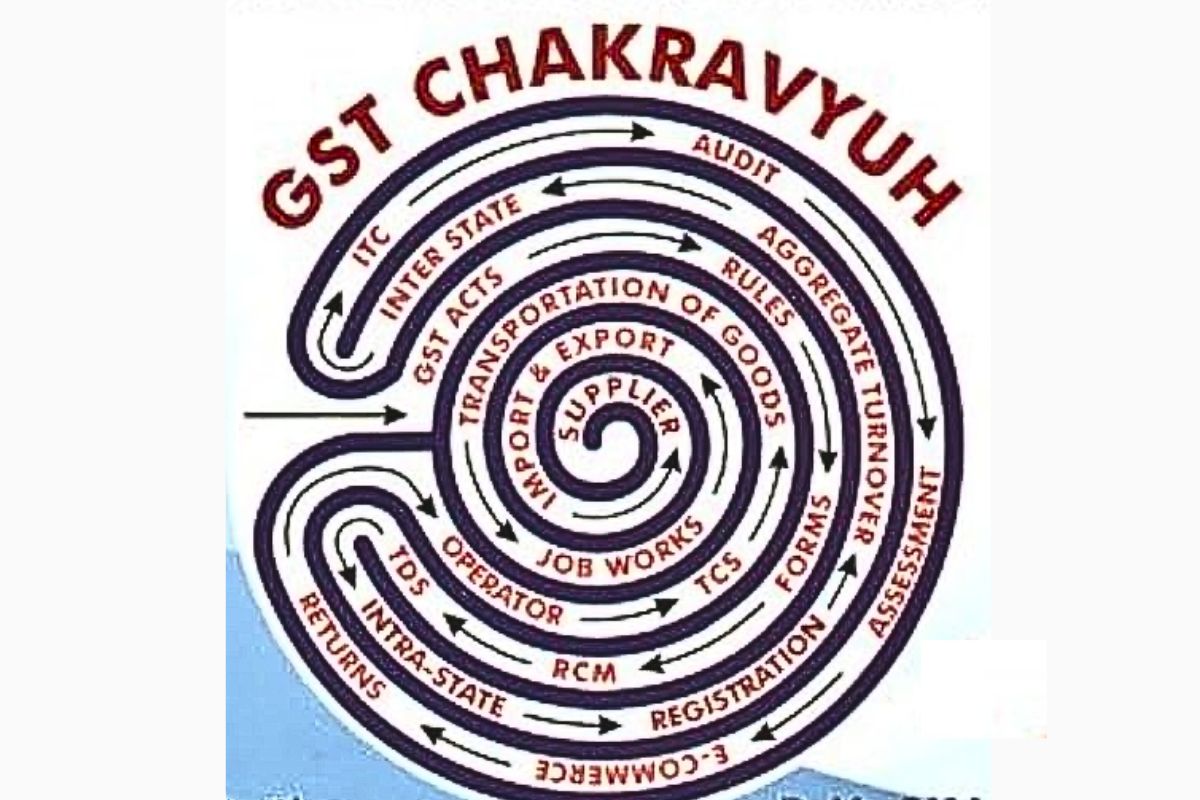

You remember what was the purpose of GST when it was introduced?

The main objective of GST was to bring the entire country under a single tax regime. It aimed to eliminate multiple layers of taxation which it has successfully done over the period of years. Along with that, another primary objectives of GST was to remove the multiplying effect of taxes. However, its seems that the purpose has been diluted and ‘WE, THE PEOPLE OF INDIA’ are again inside the ‘chakravyuh’ on GST!

The tale of Medu Vada.

A post in twitter drives you to the fascinating world of Indian tax classifications, where the difference between a plain medu vada and its curd-dipped cousin is apparently worth a 7% tax gap. Let’s dive into this perfectly logical system that only a group of distinguished “Vada Taxonomists” could devise.

- 5% GST on Medu Vada.

- 12% GST if it is dipped in curd.

- 18% GST on Curd Medu Vada with Boondi.

The GST Council, in their infinite wisdom, must have spent countless nights pondering the profound philosophical question: “When does a humble vada transcend its plain existence to become a luxury item worthy of higher taxation?” The answer, apparently, lies in those healthy bacteria in the curd that dare to make our vada more flavorful and nutritious. It seems like, how we pay different price for all the 3 varieties in a restaurant, and hence we should be ready to pay differently the taxes as well!

The tale doesn’t end here. Welcome to Chapter 2- The Popcorns!

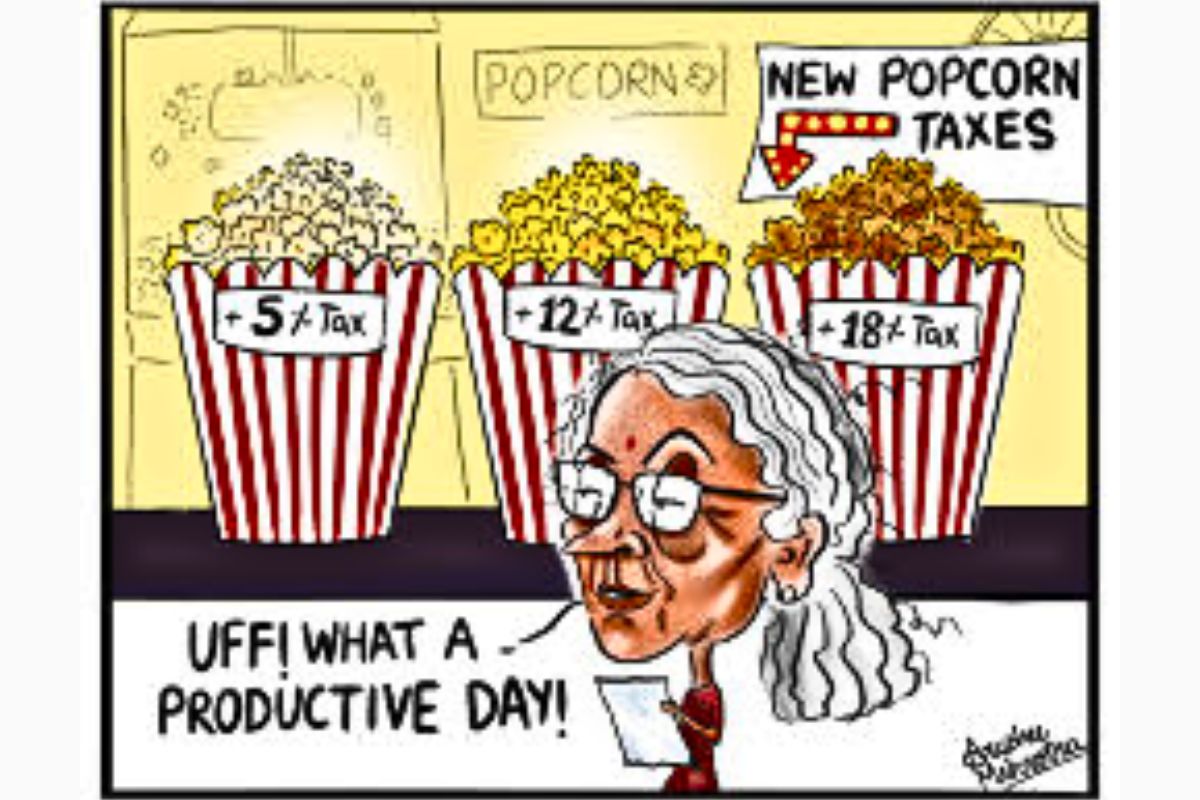

Some people consider popcorn to be one of the oldest foods in the world. That’s what the evidence from 6,700-year-old cobs with puffed kernels that archaeologists in Peru found points to. The inconspicuous popcorn did not create any commotion for the most of the time since ancient times. That is, until the Indian government decided to raise the goods and services tax (GST) on caramel popcorn from 5% to 18% last week, which sparked a lot of internet discussion.

Enters the GST Council, those brilliant taxonomists of the popcorn world! Their ability to differentiate between popcorn varieties is truly Nobel Prize worthy. Plain popcorn? Basic tax. Add brand? Different bracket. Caramel coating? Now we’re entering luxury territory! Cheese dusting? May be we would need to call the premium tax department!

One can only imagine the intense research that went into these classifications. Perhaps they have a secret popcorn laboratory where tax experts in hazmat suits study kernel transformations under different seasonings. “Alert! This batch has precisely 2.5 grams of caramel- quick, recalculate the tax liability!”

The sheer precision is impressive. It’s comforting to know that while trivial matters like healthcare and education await attention, our finest minds are ensuring that no flavored kernel escapes its designated tax bracket. Maybe next they’ll introduce sub-categories based on popping method? Air-popped versus microwave could surely justify another tax differential. And let’s not forget the potential for seasonal tax rates – monsoon popcorn clearly deserves a different treatment than summer popcorn.

Because nothing screams “economic superpower” quite like having multiple tax slabs for the same corn kernel based on what you sprinkle on top.

If you think it is just a customer’s problem, then wait. Recall how the incident from September 2024 that highlighted the problems of different GSTs in seller’s end as well. Representing the Tamil Nadu Hotels Association, Mr Srinivasan humorously criticised the inconsistent application of GST to different food items, using the cream bun as an example.

He explained that while no GST applies to a plain bun, adding cream incurs an 18% tax. “Customers now request the bun and cream separately to avoid paying the higher tax,” he said. At the very moment, his remarks were met with laughter from the audience but did not reportedly sit well with Union finance minister Nirmala Sitharaman. In a closed-door meeting the following day, Srinivasan met with Sitharaman, alongside BJP MLA Vanathi Srinivasan. A video of Srinivasan apologising to the minister later surfaced, shared by Tamil Nadu BJP functionary Balaji MS, sparking backlash on social media.

So does the purpose of GST fulfilled, or it started walking in the route of Uno-reverse?

GST, the tax system that promised simplification, ended up giving us a master’s degree worth of classifications! Nothing says “simplified taxation” quite like having different rates for the same vada or popcorn, based on whether it dared to take a dip in curd or popcorn caramelised.

Remember when they said “One Nation, One Election“? Well, they forgot to mention it would be “One Nation, One Tax, and Fifty Different Rates for Every Food Item.” Who knew we needed advanced calculus to figure out the tax on a cream bun versus a plain bun, or that popcorn could become a luxury item simply by adding caramel?

The real genius lies in turning every restaurant owner into a tax accountant. Now they must maintain separate books for plain dosas, masala dosas, and heaven forbid – premium ingredient dosas! Because clearly, the path to economic progress involves debating whether your urad dal qualifies as “premium” enough for the higher tax bracket. The economic principles at play here are truly revolutionary. It seems we’ve discovered a new law of taxation: “The fancier you think your ingredients are, the more you should pay in taxes.”

Our tax authorities have achieved the impossible – they’ve taken a system meant to simplify taxes and turned it into a byzantine maze where even determining the tax rate on a plate of vada requires a flowchart, three consultants, and possibly a PhD in “Advanced Food Classification Studies.” But hey, at least we’ve solved the crucial economic question of why a curd-soaked vada deserves a higher tax rate than its plain cousin or caramelised popcorn or it’s plain sibling. Because that’s exactly what the architects of GST had in mind, a tax system where your bill depends on whether your popcorn wore a caramel coat to the party.